As is the norm for Congress it takes a broad brush approach in solving a perceived problem without regard to the real world. This is the case with the Summary of Benefits and Coverage (SBC) required as part of Obamacare which adds more administration, more administrative costs and little additional value for consumers in making health benefit choices. This is especially true with regard to medium and large employers that now face additional regulatory burdens. The goal is to make it easier for plan participants to choose and understand their health benefits. The reality is likely to be different.

Keep in mind that since 1976 employers have been required to prepare and distribute summary plan descriptions explaining health and other benefits, but more important most employers of any size provide substantial additional information, comparison tools, interactive websites and much more to educate employees and assist them in making the right choices. The problem is and always has been not the communication provided, but the lack of attention paid to the information by employees. That is not going to change because of more federal requirements.

The individual and small group market may not have as robust communication, but isn’t that what healthcare.gov is for. Look here for the comparison of coverage available. See how clear and concise this information is. I designed and administered health plans for fifty years and these comparisons are not easy to use and only an experienced person could seek out the complete information.

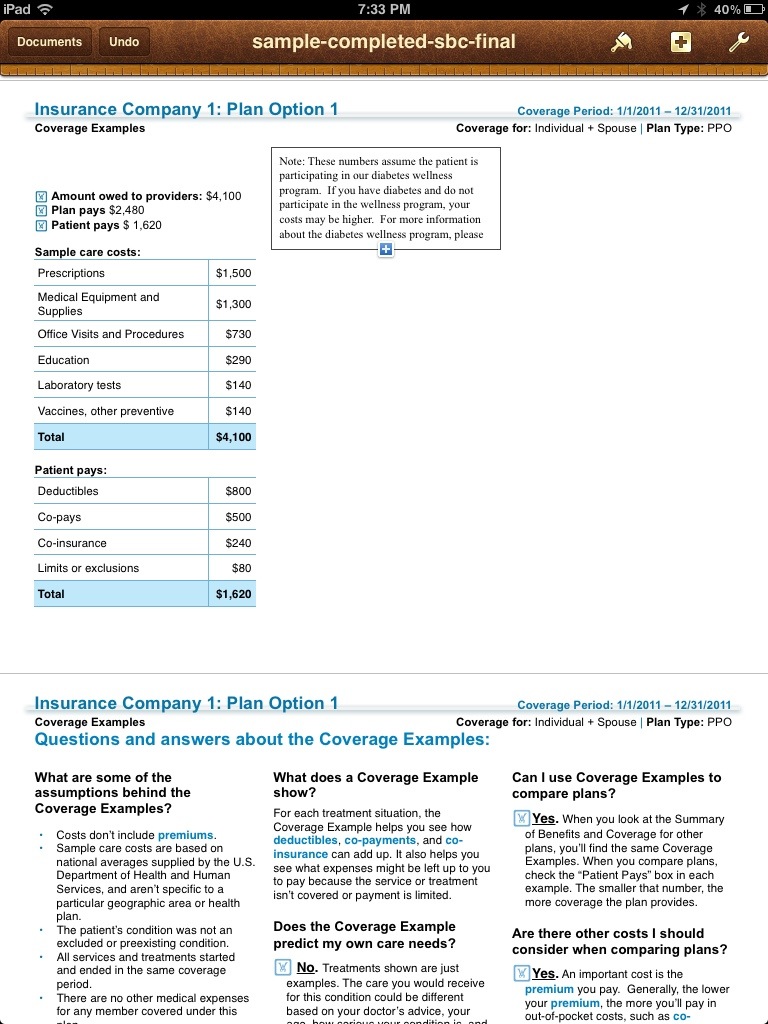

One of the most misleading aspects to SBC communication is the so-called coverage examples.

Providing an example of what will be paid for a pregnancy and treatment of diabetes can only lead to misunderstanding and unrealistic expectations. There are simply too many variables in such situations. In addition, in nearly all cases the patient’s cost is not based on the condition, but the total dollars spent in a given year. These examples may well create a new liability for employers and insurers when out-of-pocket costs do not match with the examples.

You see, despite all the rhetoric most people do not welcome an array of choices. They often overestimate their health care expenses and they fear making the wrong choice resulting in paying higher than necessary premiums. Providing more information which actually duplicates existing information in many cases does not “empower consumers to make informed decisions about their health coverage options and to choose the plan that is best for them, their families, and their business.”

Here is more of the promotion and hype from HHS:

Health care law ensures consumers get clear, consistent information about health coverage.

Because of the health care law, millions of Americans will have access to standardized, easy-to-understand information about health plan benefits and coverage. Insurance companies and employers are now required to provide consumers in the private health insurance market with a brief summary of what a health insurance policy or employer plan covers, called a Summary of Benefits and Coverage (SBC). Additionally, consumers will have access to a Uniform Glossary that defines insurance and medical terms in standard, consumer-friendly terms.

These tools will also assist employers in finding the best coverage for their business and employees.

“Thanks to the health care law, Americans will now get clear, consistent and comparable information when shopping for health coverage,” said Health and Human Services (HHS) Secretary Kathleen Sebelius. “These new tools empower consumers to make informed decisions about their health coverage options and to choose the plan that is best for them, their families, and their business.”

The SBC includes a new comparison tool, called Coverage Examples, which is modeled on the Nutrition Facts label required for packaged food, that helps consumers compare coverage options by showing a standardized sample of what each health plan will cover for two common medical situations—having a baby and managing type 2 diabetes.

The SBC will include information about the covered health benefits, out-of-pocket costs, and the network of providers. The glossary defines terms commonly used in the health insurance market, such as “deductible” and “co-pay,” using clear language.

Before today, people often lacked uniform and comparable information when shopping for coverage, often relying only on marketing materials to make decisions. Starting this fall, consumers will receive the SBC free of charge and in writing from the consumers’ insurance company or employer. This information can be requested at any time, but it will also be made available when shopping for, enrolling in or renewing coverage. It will also be provided whenever information in the SBC changes significantly.

The SBC will be available beginning today for consumers in the individual health insurance market. For enrollees in group health plans enrolling during an open enrollment period, it will be available during the next open enrollment period that starts on or after Sept. 23, 2012. For enrollees who enroll outside of an open enrollment period, it will be available at the start of the next plan year that begins on or after Sept. 23, 2012.

The SBC and Glossary were developed in collaboration with the Department of Labor, Department of Treasury, consumer groups, the insurance industry, State Insurance Commissioners, and other stakeholders.

For more information on today’s announcement, please visit:

http://www.healthcare.gov/law/features/rights/sbc/index.htmlFor a sample SBC, please see: http://cciio.cms.gov/resources/files/sbc-sample.pdf (PDF – 530 KB)

For the SBC template, please visit: http://cciio.cms.gov/resources/files/sbc-template.pdf (PDF – 475 KB)

For the Uniform Glossary, please visit: http://cciio.cms.gov/resources/files/Files2/02102012/uniform-glossary-final.pdf (PDF – 139 KB)

<;;;a

<;;/

<;;/

You state: “You see, despite all the rhetoric most people do not welcome an array of choices. They often overestimate their health care expenses and they fear making the wrong choice resulting in paying higher than necessary premiums.”

I agree in many respects. However, my experience is that people haven’t saved anything, no assets are available to meet an emergency. So, where they have a choice, they tend to select the higher level of coverage and pay higher contributions/premiums as a means of insulating them from financial shocks. They are more concerned about an unanticipated expense from point of purchase cost sharing.

Finally, one of my favorite quips is that “the only thing that is certain when you offer a choice in benefits, is that someone will make the wrong choice.”

LikeLike

Right you are. I once offered options where one became so unaffordable that we pulled it, but the unions couldn’t do it mid contract so they asked us to explain the math and try and encourage people to take another option.

One guy stopped by my office so I worked out the math and showed that what he was going to pay in premium was always going to be considerably more than any possible out of pocket costs under any conditions. He finally saw my point and said he was switching.

The next day he came back and said he talked to his wife and they decided to stick with the “Cadillac” plan. That decision cost them over $1,000 a year.

Dick

Richard D Quinn Editor

http://www.quinnscommentary.com

Health Insurance Illuminated http://blog.horizonblue.com/

LikeLike