I have often said the idea of provider networks with all their cost to maintain and their complexity to administer is a waste of money.

Better for an insurer to set its reimbursement amounts, let consumers know and then consumers can shop for a physician who will accept the fee payment (or not); the good old days when plans used fee schedules. Instead, in another attempt to control costs many insurers are shrinking networks thereby giving patients less choice of providers and greater risk of paying penalty level coinsurance.

Using out of network providers by choice or chance is unfair to everyone, the patient and all the other customers of the insurer who may end up paying these costs through their premiums.

State regulations make the issue more complicated and sometimes unfair.

The system is simply ass backwards especially when one considers that being a participating provider means little beyond accepting a “negotiated” fee. And yet we still have HHS spokesmen saying things like this:

A spokesman for the Department of Health and Human Services said “consumers will find a range of quality, affordable coverage options on the Marketplace in 2016.” WSJ 9-4-15

What exactly is quality coverage? And what is “affordable?”

Try disputing a service provided by a participating doctor and deemed medically unnecessary or inconsistent with accepted medical practice by the insurance company. You will quickly learn there is no relationship between participation and any guarantee of accepted health care claims or relationship between the way a given doctor practices medicine (quality) and insurance company rules.

Besides, what point is there to contracts between an insurer and physician if state law simply overrides the payment process? See below. Regulators see themselves fighting for the consumer and ignore the fact all costs they mandate will be paid by consumers, just ones different from the individual involved in a given claim.

The following is an excerpt from Kaiser Health News 8-19-15

What Some States Are Doing (about out-of-network charges).

While patients may be on the hook for these bills, about a quarter of states have enacted protections, mostly for emergency room situations. A Kaiser Family Foundation analysis in 2013 noted that 13 states have some kind of restrictions on balance billing patients in certain situations.

“If you ask the insurance and physician community, they would say they’d love to keep patients from being caught in middle,” says Jack Hoadley, a research professor at Georgetown University’s Health Policy Institute who’s examined policies in seven states. “But until they can agree on how payments are worked out between the insurer and physician, it’s hard to get legislation passed.”

In Colorado, insurers must pay non-network providers what the providers charge patients at in-network hospitals or what they’re willing to negotiate. Under HMO plans in Florida, on the other hand, Hoadley says providers cannot bill for more than what an insurer agrees on. And insurers in Maryland must pay for covered services at rates the state sets.

Transparency in pricing is also an issue: California has rules mandating that certain insurers maintain accurate in-network provider lists. Texas has a mediation process for certain types of surprise bills and the governor there recently signed a law providing more price and network transparency at free-standing emergency facilities.

New York’s New Law ‘Already At Work’

The state enacted legislation this spring that provides more transparency around what services cost and safeguards patients when they do get a surprise bill. Under the rules, if patients don’t know in advance that a doctor is out of network or if they have no choice, they won’t be responsible for the bill. Instead, it’s up to the insurer and provider to reach a payment deal through an independent resolution process.

“The broad principle is people who do everything right to stay in network, but get slammed with bills, they are going to be held harmless,” says Matthew Anderson, a spokesman for New York’s financial services office. “It’s already helping consumers. It’s a really great relief to those who otherwise would have been fighting for years with their insurance company over these bills that run into the tens of thousands of dollars.”

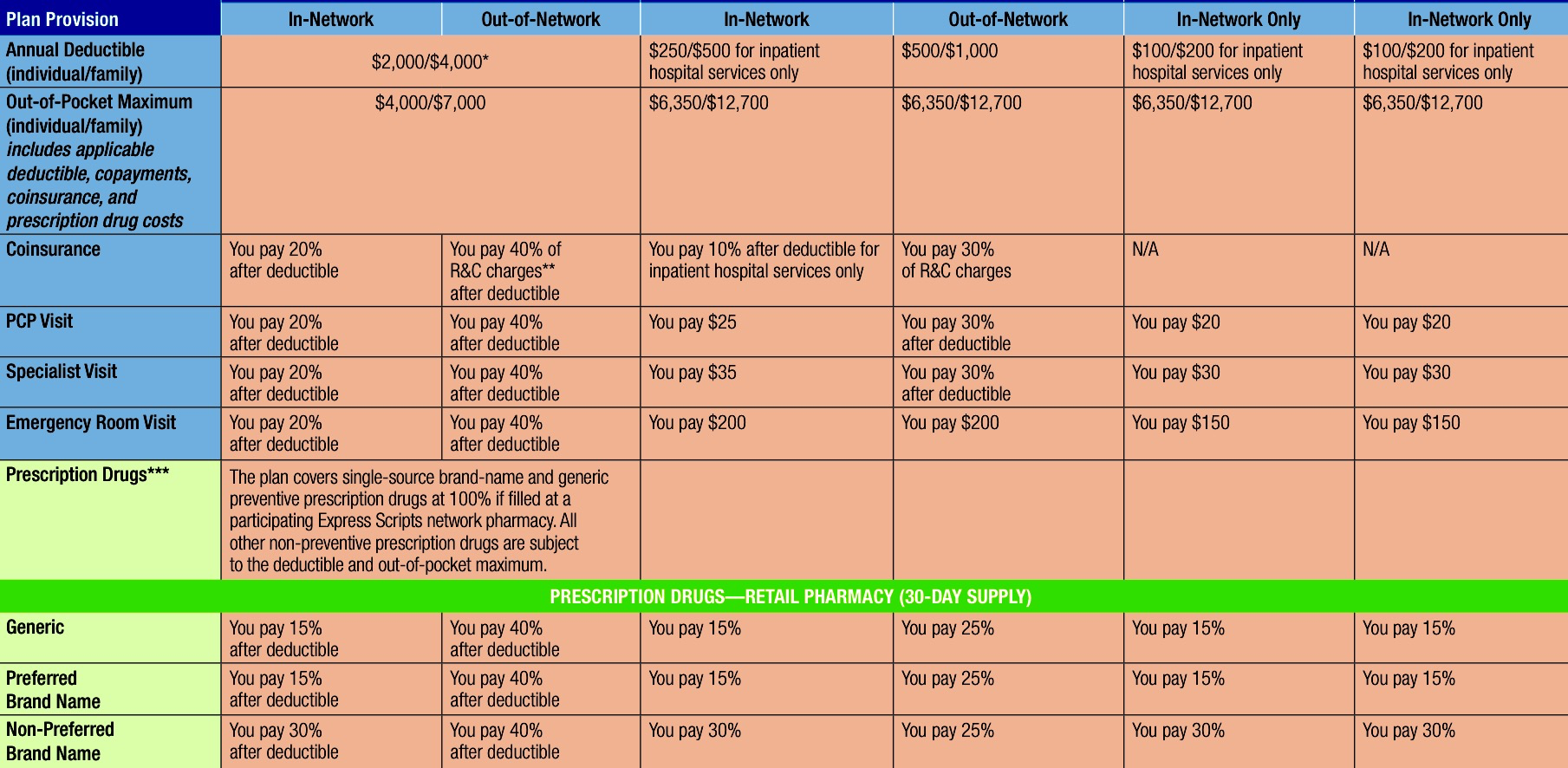

Enter employer plans (and Obamacare exchanges for that matter) and the patient is confronted with choice and complexity that is unnecessary. Here is an example. I ask you, who can remember all this? Some options are in-network only, do you pay 20%, 40%, 30%, 15% or 25%?

Look at the out-of-network coinsurance for the high deductible plan on the left. Do you think 40% coinsurance after a $4,000 deductible is affordable for most families? Do you think such barriers could prevent some families from receiving the highest quality health care or any needed health care?

Now consider all this from the provider perspective. Do you seriously believe a doctor can keep track of all the different rules and fees from a score of insurance plans in which he may “participate?” Do you believe it is anything more than a ridiculously complex payment mechanism?

We may value freedom of choice, but wouldn’t it be more logical, efficient and fair if everyone knew that the allowable fee for an office visit was $50 or a MRI was reimbursed at $350 no matter your insurance? Health care providers could charge what they wanted and patients could decide who to use, no questions asked. The competition element would be on health care providers where it belongs for cost, quality and efficiency.