Next year about one-third of large employers will make only a high-deductible health plan available to employees. More will make such a plan an option; generally with financial incentives to enroll.

The bottom line is that employers have found a politically correct way to shift massive costs to workers. Why politically correct? Because they take cover under the buzz words of “consumer driven.” The idea being that patients faced with upfront costs will be more prudent shoppers of health care, thereby helping to control costs … yeah‼️

If you read this blog regularly, you know how I feel about all this. If not, read this.

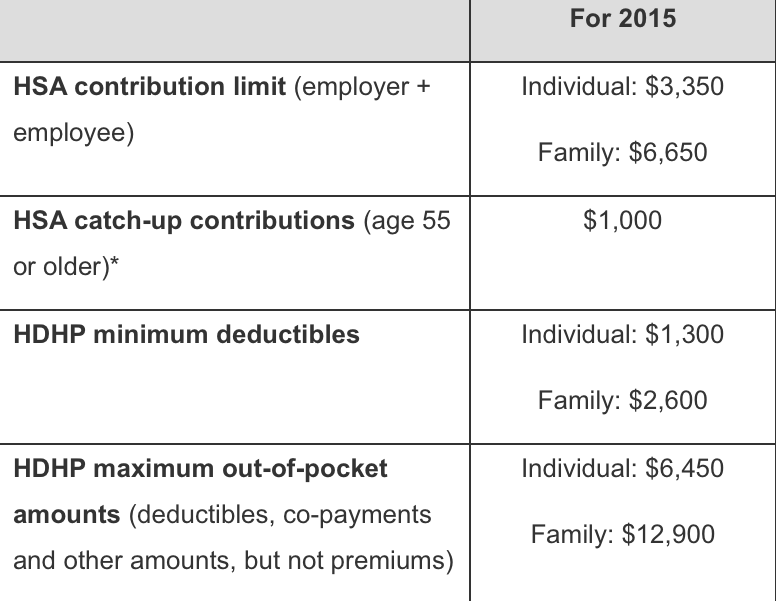

The fact is the HDHP places a heavy financial burden on families, especially lower-income families. In an era of stagnant wages, this blatant cost-shifting can hurt. Sure, a HDHP means lower monthly contributions for employees and if you have few or no health care expenses all is well, but on the other hand, you must be prepared to come up with the cash to cover the deductible. The 2015 minimum for a qualified HDHP is $1300 for an individual and $2600 for a family; some plans require a higher deductible. The minimum increases each year based on IRS regulations.

The other part of the story is the ability to pre-fund your out-of-pocket costs via a Health Savings Account (HSA). There are many advantages to such a plan, but you must come up with the cash to fund it (some employers will make a contribution as well), and for many people that’s not so easy when the same discretionary cash must also fund retirement savings.

However, even if you place $100 a month in your HSA, that will be small comfort if your child falls in the playground and the bills in January come to $3,000 – you can’t use the HSA until all the cash is in the account. You must come up with at least $2600 for the deductible, maybe more.

Whether all this cost shifting turns patients into conscientious consumers or just paupers is open for debate (not much though). However, it certainly makes family finances more difficult. Of course, you can just not go to the doctor😢

Bottom line; patients are being asked to do what the health care system should be doing and that is providing coordinated, efficient health care in the right setting, at the right time and at the appropriate level. Got all that Mr. Consumer Patient⁉️

Today’s $1,300 is no larger a percentage if health costs than my $100 deductible thirty years ago. It is a misnomer to call that high.

LikeLike

True in relative terms, but that’s not much comfort to the worker who next open enrollment sees his POS gone and instead faces a $4,000 family deductible.

LikeLike

When I started in benefits in 1961 we had a $100 deductible on major medical only. Today that would equal $795.49. On the other hand I recall $5.00 office visits which today would be $39.77 in general CPI increases. Interestingly, today Medicare allows less than that for many office visits. As we know, the increase in health care is not so much unit prices but utilization and technology.

LikeLike

What rate did you use, the CPI? I used actual rates from 1984 to 2014, and my $100 increased to over $1,600 – an annual average of just under 10 percent

– doubling four times in 30 years

LikeLike

Yes, CPI

LikeLike