We can’t control what others do and we can’t stop misfortune from striking. But we can control our own actions. Those who are financially prudent will most likely enjoy success, even if events don’t always go their way.

I find the Committee for a Responsible Federal Budget a reliable source of information on federal budgets and spending. I share their information as a source to help understand what may be muddled in the political arena. Nearly all presidents in modern times have added to the deficit.

Doing so in the face of a national emergency is one thing, doing so on a regular basis to avoid the truth about spending and taxes is quite another.

In the recent GOP primary presidential debate, Ambassador Nikki Haley claimed that President Trump added $8 trillion to the national debt while Florida Governor Ron DeSantis said that President Trump added $7.8 trillion to the debt. These statements are true, depending on how you measure additions to the debt. We estimate the ten-year cost of the legislation and executive actions President Trump signed into law was about $8.4 trillion, with interest.

It’s also the case that the government accumulated $7.8 trillion of gross federal debt while President Trump was in office, though much of this is unrelated to President Trump’s actions.

US Budget Watch 2024 is a project of the nonpartisan Committee for a Responsible Federal Budget designed to educate the public on the fiscal impact of presidential candidates’ proposals and platforms. Through the election, we will issue policy explainers, fact checks, budget scores, and other analyses. We do not support or oppose any candidate for public office.

There are at least two ways to measure how much President Trump added to the debt – though coincidentally they lead to similar conclusions of about $8 trillion.

One way to measure how much President Trump borrowed is by estimating the debt accumulated over his presidency. Over the course of President Trump’s four years in office, the gross national debt grew from $19.95 trillion to $27.75 trillion – a $7.8 trillion increase (debt held by the public – the more economically-meaningful measure of debt – grew by $7.2 trillion over this period).

However, much of this borrowing was due to policies put in place before President Trump took office or due to unexpected changes in circumstance. Debt was already projected to grow by about $3 trillion for the four years of his term when President Trump took office, and some of the additional debt accrued was also the direct result of the COVID-19 pandemic and recession. It’s also important to note that the government was holding an unusually large $1.6 trillion in cash when President Trump left office, which inflated the growth in debt relative to the deficit run during his time in office.

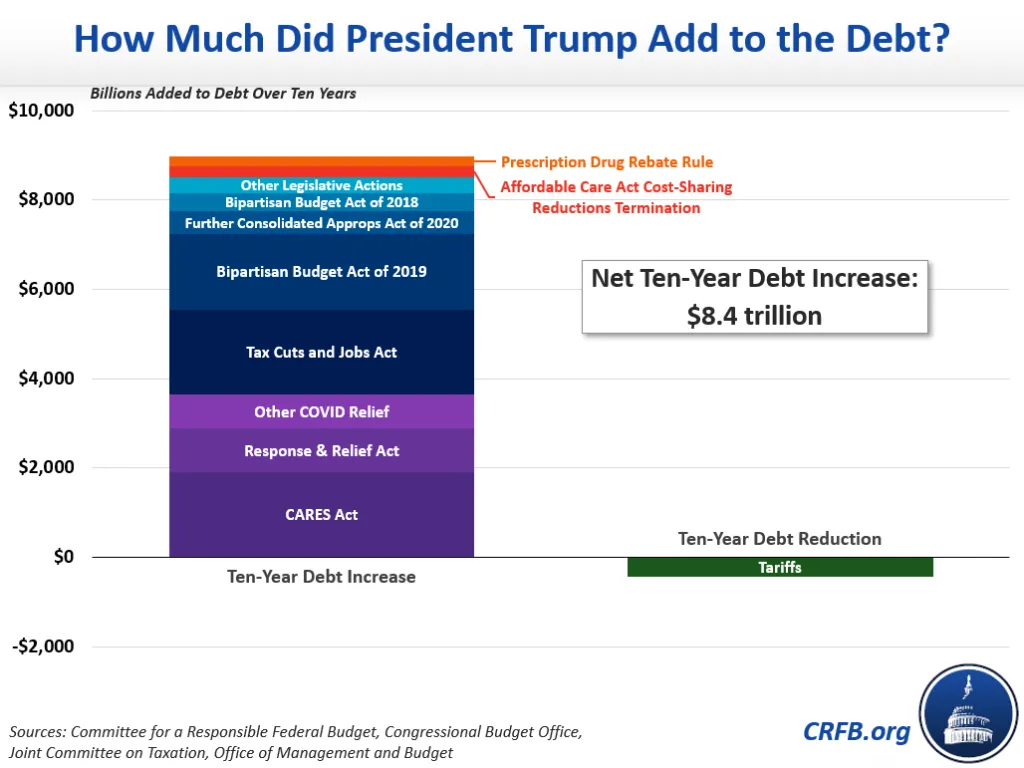

A better way to measure how much President Trump added to the debt is to evaluate the ten-year debt impact of the laws and executive orders he signed. We estimate that those added a combined $8.4 trillion to the debtover a ten-year period – consistent with Haley’s claim.

On net, almost all of the $8.4 trillion in ten-year debt approved by Trump came in the form of legislation, with costly executive actions largely offset by a unilateral expansion of tariffs. It included $8.8 trillion of net increases in the debt and $445 billion of net reductions. $7.3 trillion represents an increase in primary deficits, and $1 trillion comes from interest costs.

Of the $8.4 trillion President Trump added to the debt, $3.6 trillion came from COVID relief laws and executive orders, $2.5 trillion from tax cut laws, and $2.3 trillion from spending increases, with the remaining executive orders having costs and savings that largely offset each other.

The largest bills include $1.9 trillion from the 2020 CARES Act, another $1.9 trillion of ten-year borrowing from the 2017 Tax Cuts and Jobs Act, and a further $2.1 trillion of borrowing from the Bipartisan Budget Acts of 2018 and 2019, which mainly increased discretionary spending. The bipartisan Further Consolidated Appropriations Act of 2020 enabled an additional $500 billion of borrowing, mainly from the repeal of various Affordable Care Act (ACA) taxes and other bipartisan tax cuts. Other significant legislation added a combined $350 billion to the deficit.

In terms of executive actions, President Trump’s unilateral expansion of various tariffs raised about $445 billion over ten years, largely offsetting the cost of other actions such as the termination of the ACA’s cost-sharing reductions funding and a prescription drug rebate rule (which was ultimately repealed).

Tax and Spending Laws$4.8 trillionTax Cuts and Jobs Act$1.9 trillionBipartisan Budget Act of 2018$420 billionBipartisan Budget Act of 2019$1.7 trillionFurther Consolidated Appropriations Act of 2020$500 billionOther Legislative Actions$350 billion

Executive Actions$10 billionTariffs-$445 billionAffordable Care Act Cost-Sharing Reductions Termination$250 billionPrescription Drug Rebate Rule$205 billion Total$8.4 trillion

Tagalog Excluding COVID Relief$4.8 trillion

Sources: Committee for a Responsible Federal Budget, Congressional Budget Office, Joint Committee on Taxation, and Office of Management and Budget. Note: figures may not sum due to rounding.

To be sure, other Presidents have also added substantially to the debt. In a future analysis, we will estimate how much President Biden has added to the debt – we pegged this figure at $4.8 trillion before the passage of the Fiscal Responsibility Act and other recent actions.

Importantly, President Trump also proposed substantial deficit reduction inhis variousbudgets. However, almost none of these savings were enacted into law.

If about 49% of the folks pay no federal income tax programs will multiply once they realize almost half the country will pay nothing. Sounds good and make sense: if you want it pay for it. What sounds better is I want it and brother Quinn pays for it.

Well that’s simple–the world economies had similar tax rates–at some point corporate tax rates began to decline in order to create an advantage for firms doing business–all you have to do is GOOGLE global corporate tax rates–we are now right in the middle–some countries higher–some countries lower–but we are much lower than we were say in 2014.

I believe Ireland taxes at 15%–taxes are a cost of doing business–if our rates are 30% federal and say 10% state it is going to make a big difference. Just an article in the WSJ about how Germany’s economic growth has really taken a hit–also mentioned is since 2017 the U.S. economy has been far stronger with more growth than most European nations–lower taxes has been a prime driver in my opinion.

Yes, personal rates were in the range of 70% maybe in the Eisenhower years–but nobody paid that–there were all kinds of deductions–who in their right mind would pay, on the last $ of earnings, 70 cents out of every dollar? Ask yourself a simple question–why are so many people fleeing high tax states? States with low rates are seeing population growth–states with high taxes in many cases see low growth and/or economic stagnation.

Neither Trump or Biden will do anything about deficit spending if either is in office during the next four year term. That much is a certainty. How you vote depends on how you view other issues.

Tax increases probably, especially since the Trump tax package has a sunset clause. The new Congress won’t be chomping at the bit to make everyone mad about higher taxes but they will raise taxes before they cut spending. The President will go along and will try to place blame on someone else.

What is interesting is that of the few policies that the Trump campaign have floated so far, for his potential next term, all are both inflationary and would greatly increase the debt, including more tax cuts for the rich, tariffs, and causing wage inflation by eliminating workers for key industries like construction. If someone supports MAGA because they are against abortion, that is a legitimate stance, but anyone who claims to support MAGA because of fiscal or economic management is either ignorant or willfully deceiving themselves.

First Trust–Monday Morning Outlook has a good piece dated 01/16/24. Non defense spending (SS/Medicare as an example) was 10% of GDP in the ’60ies–15.2% of GDP in ’07–17.8% of GDP in 2019 and 27.7% of GDP in 2020. The projection is 22% for next 5 years.

Government takes more and more of what private sector produces and annual deficits of $2 trillion is predicted.

Voting for the same folks will give us the same results.

Net interest expense of $332.6 billion in 2020–past 12-months $703.4 billion.

Raise taxes? Between 1998 and 2001 we had a budget balances and tax receipts were 19.4% of GDP–total spending 18% of GDP.

In the 1980’s and 1990’s when we cut spending real GDP grew at an average of 3.2% annually. Past two years the average is 1.7%.

Last year CBO overestimated tax revenues by 11% and underestimated spending by 9%.

If the economy is humming along according to some and we are running huge deficits what happens when the economy slows?

Cut spending and good things can happen–we are bringing in more money than ever but running large deficits not a surplus.

In our younger years we might have suffered a job loss. At the kitchen table many folks immediately worked on a budget that primarily looked at where we could cut spending. Seems like common sense.

I agree. Raising taxes and cutting deficit spending during a boom times is good fiscal policy. The problem is that there are no viable candidates running for office that support this. Our tax rates are some of the lowest in history right now. And where to cut spending, as the choices are basically defense, Medicare, or Social Security, all of which are untouchable… the only viable answer is immigration to grow our tax base and make our overall population younger.

Good points–what we need of course is a rational immigration policy and welcome folks coming here legally.

You can raise taxes to the moon and all you get is a stagnant economy. If high taxes are a solution someone explain why so many blue states are bleeding people and the budget deficits are large via the GDP of those states.

If you try and “tax the rich” the wealthy folks of NJ–NY–Ct–MA–DC–CA and on and on complain. You know we have the $10,000 maximum tax deduction for such things as giving and property taxes. The wealthy screamed like crazy. Taxing the rich did not mean them. It’s always someone else.

You mean a “flat” tax?? Taxes are never level. Liquor taxes are more than “ordinary” sales taxes–taxes on guns are different than taxes on shovels. Taxes on cigarettes we know are out of sight.

If about 49% of the folks pay no federal income tax programs will multiply once they realize almost half the country will pay nothing. Sounds good and make sense: if you want it pay for it. What sounds better is I want it and brother Quinn pays for it.

LikeLike

I would love to hear Al Lindquist explain why America thrived in the 20th century with much higher tax rates.

LikeLike

Well that’s simple–the world economies had similar tax rates–at some point corporate tax rates began to decline in order to create an advantage for firms doing business–all you have to do is GOOGLE global corporate tax rates–we are now right in the middle–some countries higher–some countries lower–but we are much lower than we were say in 2014.

I believe Ireland taxes at 15%–taxes are a cost of doing business–if our rates are 30% federal and say 10% state it is going to make a big difference. Just an article in the WSJ about how Germany’s economic growth has really taken a hit–also mentioned is since 2017 the U.S. economy has been far stronger with more growth than most European nations–lower taxes has been a prime driver in my opinion.

Yes, personal rates were in the range of 70% maybe in the Eisenhower years–but nobody paid that–there were all kinds of deductions–who in their right mind would pay, on the last $ of earnings, 70 cents out of every dollar? Ask yourself a simple question–why are so many people fleeing high tax states? States with low rates are seeing population growth–states with high taxes in many cases see low growth and/or economic stagnation.

LikeLike

How much have Dems and Biden added? I guess the Dems were AWOL when Trump added all those deficits.

LikeLike

This is a useful explanation of an important topic. We mostly hear soundbites rather than clear discussions like this. Thanks.

LikeLike

Neither Trump or Biden will do anything about deficit spending if either is in office during the next four year term. That much is a certainty. How you vote depends on how you view other issues.

LikeLike

Depends on the balance of the new Congress. I see tax increases. It’s inevitable.

LikeLike

Tax increases probably, especially since the Trump tax package has a sunset clause. The new Congress won’t be chomping at the bit to make everyone mad about higher taxes but they will raise taxes before they cut spending. The President will go along and will try to place blame on someone else.

LikeLike

What is interesting is that of the few policies that the Trump campaign have floated so far, for his potential next term, all are both inflationary and would greatly increase the debt, including more tax cuts for the rich, tariffs, and causing wage inflation by eliminating workers for key industries like construction. If someone supports MAGA because they are against abortion, that is a legitimate stance, but anyone who claims to support MAGA because of fiscal or economic management is either ignorant or willfully deceiving themselves.

LikeLike

First Trust–Monday Morning Outlook has a good piece dated 01/16/24. Non defense spending (SS/Medicare as an example) was 10% of GDP in the ’60ies–15.2% of GDP in ’07–17.8% of GDP in 2019 and 27.7% of GDP in 2020. The projection is 22% for next 5 years.

Government takes more and more of what private sector produces and annual deficits of $2 trillion is predicted.

Voting for the same folks will give us the same results.

Net interest expense of $332.6 billion in 2020–past 12-months $703.4 billion.

Raise taxes? Between 1998 and 2001 we had a budget balances and tax receipts were 19.4% of GDP–total spending 18% of GDP.

In the 1980’s and 1990’s when we cut spending real GDP grew at an average of 3.2% annually. Past two years the average is 1.7%.

Last year CBO overestimated tax revenues by 11% and underestimated spending by 9%.

If the economy is humming along according to some and we are running huge deficits what happens when the economy slows?

Cut spending and good things can happen–we are bringing in more money than ever but running large deficits not a surplus.

In our younger years we might have suffered a job loss. At the kitchen table many folks immediately worked on a budget that primarily looked at where we could cut spending. Seems like common sense.

LikeLike

I agree. Raising taxes and cutting deficit spending during a boom times is good fiscal policy. The problem is that there are no viable candidates running for office that support this. Our tax rates are some of the lowest in history right now. And where to cut spending, as the choices are basically defense, Medicare, or Social Security, all of which are untouchable… the only viable answer is immigration to grow our tax base and make our overall population younger.

LikeLike

Good points–what we need of course is a rational immigration policy and welcome folks coming here legally.

You can raise taxes to the moon and all you get is a stagnant economy. If high taxes are a solution someone explain why so many blue states are bleeding people and the budget deficits are large via the GDP of those states.

If you try and “tax the rich” the wealthy folks of NJ–NY–Ct–MA–DC–CA and on and on complain. You know we have the $10,000 maximum tax deduction for such things as giving and property taxes. The wealthy screamed like crazy. Taxing the rich did not mean them. It’s always someone else.

LikeLike

Tax levels need to equal at least the cost of programs and services people need and want.

LikeLike

You mean a “flat” tax?? Taxes are never level. Liquor taxes are more than “ordinary” sales taxes–taxes on guns are different than taxes on shovels. Taxes on cigarettes we know are out of sight.

LikeLike