Let me see if I have this right, if you and your long-term partner who bought a house together and have been living together each earn $199,000 a year you are not wealthy. If you and your partner marry, you instantly become wealthy because your “family” income equals more than $250,000.

If you are single and earn $200,000 a year you are wealthy. If you marry and still earn $200,000 you are not wealthy. If you earn $125,000 a year and your girlfriend earns $125,000 a year neither of your are wealthy, but if you get married your family is now wealthy because you earn $250,000.

If you win $50,000,000 in the lottery, you are wealthy the year you win, but if you put your money in the bank and earn a mere $125,000 in interest, you are no longer wealthy.

To go from single to married only requires a bump in income of 25% or $50,000 to be wealthy, not double as logic would dictate. Wait, in fact it’s more than logic, it’s the law. When Medicare determines the level of supplemental Part B premiums for high income beneficiaries the income levels for those filing joint income tax returns are exactly double the amount for the single filer.

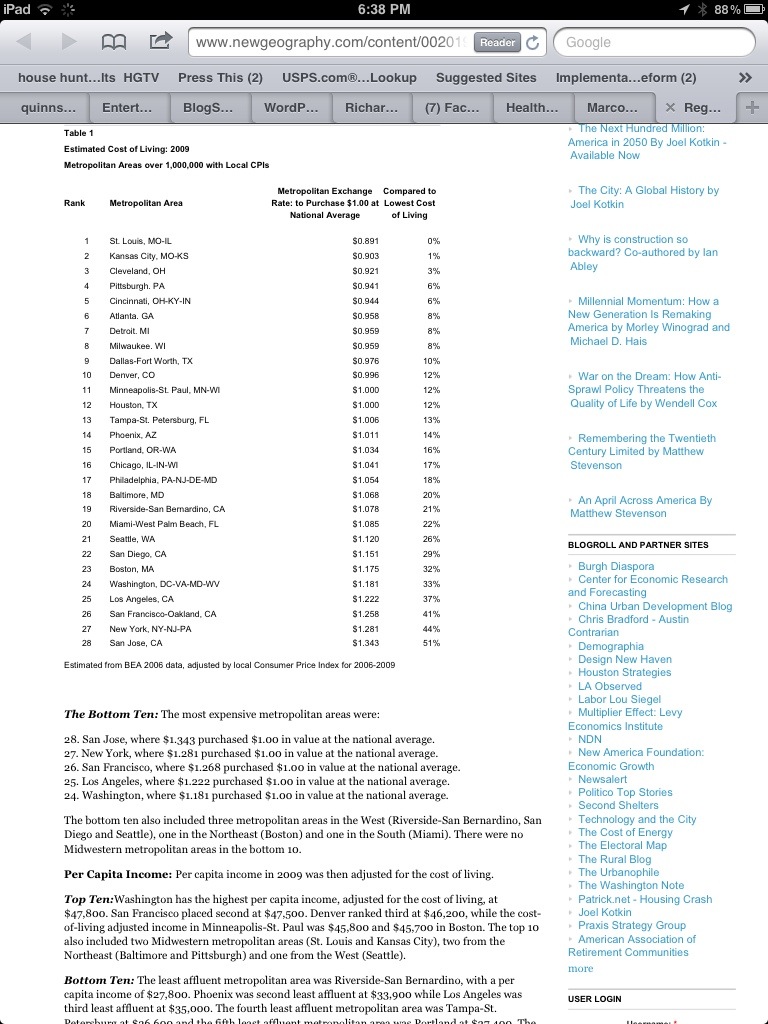

Then we have the U.S. exchange rate. That is simply the variation in cost of living in areas of the country. For example, if you earn $250,000 in New York you only really earn $180,000 when compared with the national average for the cost of living. In other words it takes 28% more income to live comparatively in the NY, NJ region. So, if you are wealthy in the South or Mid-West, are you still wealthy in North Jersey? Ah, not so much.

And what is the point of all this? Who the heck knows? However, it seems to me we should think things through carefully before we rush to change tax rates that lump all the so-called wealthy into one clump that includes the likes of Buffett and company.

Everyone seems to have bought into the tax increase idea without asking how we can be sure that every penny of new revenue reduces the deficit. That fact is past experience tells us Congress will find new ways to spend everything going into federal coffers. As the economy recovers and GDP growth gets back to normal, revenue will naturally go up. Spending, not revenue, is the real problem and always has been. But you see the tax message is much easier to deliver especially if they convince you someone else will be affected. When you tell people the truth about spending and the unaffordable promises made, you get the AARP, unions and others organizations protesting in the streets and telling you no cuts are necessary.

Perhaps it’s time to give up; raise all tax rates with a top of 90% like the good old days. Provide Americans with Social Security, free Medicare, Medicaid, all health care, free college and day care, paid family leave and food stamps … or we could all just move to France … wait, they’ve done this and it doesn’t work. Now what?

Related articles

- Obama: Wealthy must pay more tax (bbc.co.uk)

- CBO says tax hike for wealthy will hurt growth (aei-ideas.org)

- Changing America – raising taxes (on somebody else) is our salvation (quinnscommentary.com)

My second comment is that I think the $250K and $200k limit is based on some percentage – 98% of married people make less than $250k and 2% of singles make less so lets set those numbers. What was failed to be reviewed was the fact that there should be a coorelation between the numbers such as $250K for married people and $125K for singles. Maybe you argue that married people have savings by joint household etc but then change it to $150K vs $250K. I am fine paying the extra tax (honestly I am) but I am NOT fine knowing that I will save money on taxes (significant amounts) if I divorce my wife…..

LikeLike

This article is 100% what I have been saying since the original proposal but I will add a few more items to it. This $250K / $200k rule is hitting the hardest on those that are trying to have two careers.

First of all if you have two people making say $125K each neither one would be deemed rich as singles but they would be deemed rich as married. Compare this to the “old traditional” one person makes the $250K and one is stay-at-home.

Secondly married successful people are already paying more in SS taxes than the “traditional”. If you are married and one person makes $250,000 and the other person is at home then you are paying Social Security taxes on approximately $110K of your income. If you are married and you are both making $125K then you are paying Social Security taxes on $220K of the family income….. in both cases when you reach an age where you can benefit from the system you will get the same amount.

Me and my wife cannot deduct any of our student loan costs since we make too much, we have over $15K in daycare bills / year and only $6,000 is deductible (we have daycare so we can work), one of us is often working weekends / nights and the other one has the kids. We prioritize our children but set a good example by working hard and they only go to day-care about 25% Monday-Fridays.

We live in a high-cost state and now we are going to be deemed rich. If we got divorced we would as individuals both be under the $200k limit

LikeLike

Another good post Mr. Quinn. It points up the need for true tax reform and how illogical our current system is. The $200,000 for single and $250,000 for married definition of wealthy were arbitrary assumptions based on nothing concrete.

Actually, current year income as a measure of wealth is highly illogical because it does not account for owned assets. The whole idea that we of tax ourselves by wealth is a myth.

Our country’s system of raising revenue is for the most part annual income based. That includes individual income tax, corporate tax and FICA (social security and Medicare).

Additional illogicals are placed in our income based tax laws by the Congress critters to garner “re-elect me favors” from special interest groups. The illogicals I refer to are loopholes, deductions, tax expenditures, tax preferences or any other name they masquerade under.

It is common to focus attention on corporate tax loopholes because they are an easy mark but that’s not where the real money is. The real money is in individual tax deductions. One example is the mortgage interest deduction. It is said that this deduction is sacrosanct and it will never be repealed. It was one of the few individual deductions that survived the 1986 tax reforms. In survey after survey, the American public when asked agrees that the mortgage interest deduction is a good thing but only 22% can take the deduction with most of the benefit going to high income individuals. What is logical about that?

Each loophole has its own supporters and self interest group who will come up with reasons why their favorite loophole is good for society at large but what we have to ask ourselves is it logical?

As you have mentioned many times in this blog, there is no free stuff, it only seems that way when someone else is paying. Tax breaks are not free; everyone else has to pick up the tab.

LikeLike

You are right about most of the so called loopholes going to the middle class. In fact the largest revenue loser in this category is the tax free status of employer contributions for health care benefits.

Dick

Richard D Quinn Editor

http://www.quinnscommentary.com

Health Insurance Illuminated http://blog.horizonblue.com/

LikeLike

Here is another interesting twist on employer sponsored health care benefits. The employers with the highest cost plans paying the highest percentage of premium are federal, state, city, and municipal governments.

We see it all the time: workers for private employers pay a large percentage of premium for bare-bone plans, while government workers pay almost nothing for Cadillac plans.

As costs of these benefits have climbed over the years, the cost of employing government workers have climbed in unison. Healthcare premium contributions are not counted as income. If they were, more government employees might be counted as weathy.

LikeLike

Interesting point and quite true.

Dick

Richard D Quinn Editor

http://www.quinnscommentary.com

Health Insurance Illuminated http://blog.horizonblue.com/

LikeLike