You will hear advice on beginning Social Security that goes from start at age 62 to wait as long as you can. The choice you make will affect the amount of your monthly benefit and the total amount you receive in your lifetime. You must decide which is most important to you.

If you are one of the fortunate Americans to have a pension, you may also be faced with the decision to take either a life annuity or a lump sum payment of the value of your pension.

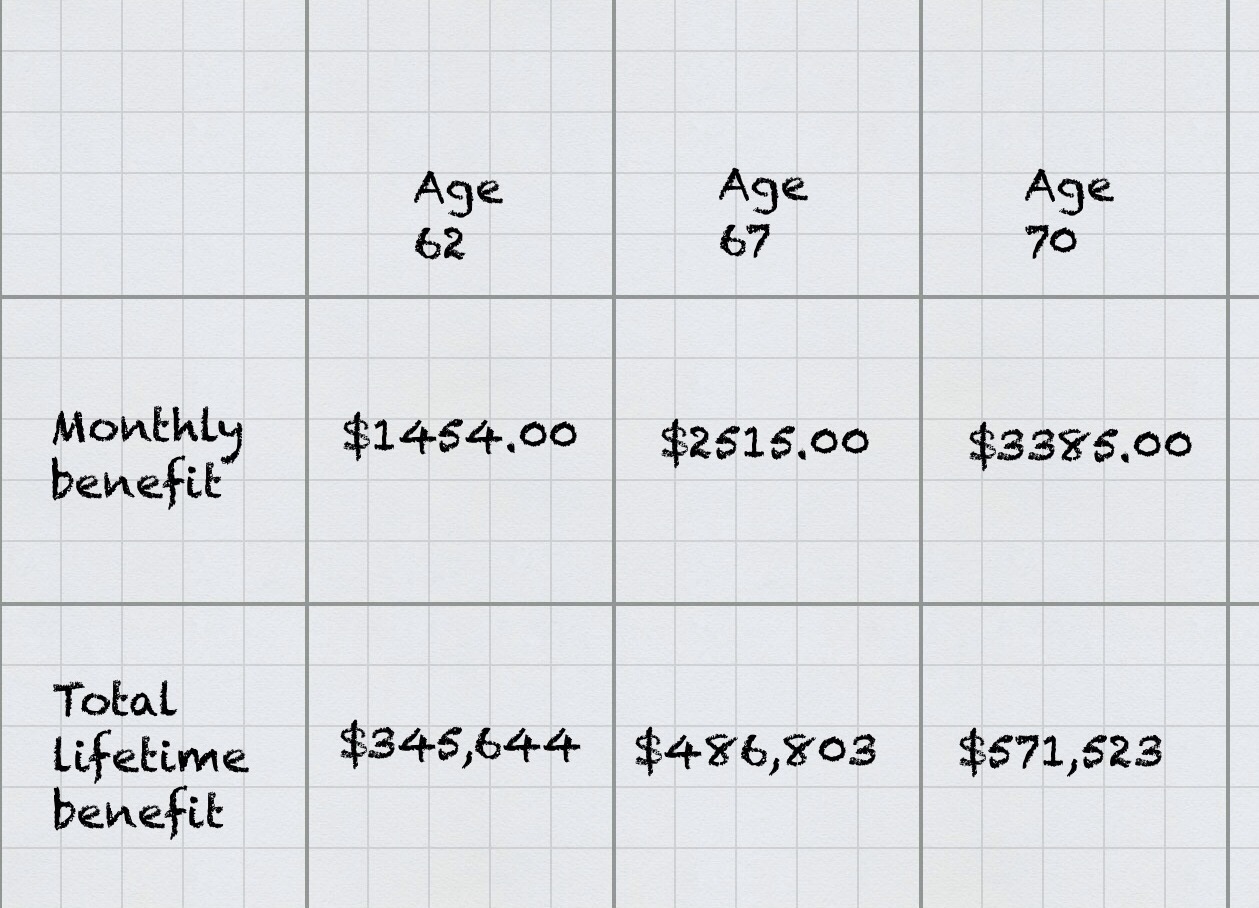

Let’s look at a Social Security example. You were born in 1952, in 2013 your income was $80,000. Using the Social Security Quick Calculator and the Social Security actuarial life expectancy tables, you get the following numbers. At age 62 life expectancy is 19.81 years, at 67;16.13 years and at 70;14.07 years. In any case, if you make it this far, you are on your way to being an octogenarian.

[Note the total payment amount assumes you live to your full life expectancy. These amounts do not include a spousal benefit which could add 50% more to the monthly benefit while the primary beneficiary is alive. Also, all amounts are in inflation adjusted future dollars.]

So, what is the best age to begin Social Security? There is a very easy answer; it depends! If you need the money, start at age 62 recognizing there is a significant reduction in benefits. If you live to your full life expectancy you will receive less in total than if you waited until age 70, but if you only live say ten years that changes. Do you care about the total benefits you collect over your lifetime or do you care more about maximizing your monthly income? That’s the real choice. But the choice must look at the future as well. Even though Social Security has a built-in COLA, time will erode the value of your income. That means the more income you have to begin with even if it is more than you need today, the better off you will be in the years ahead.

If you haven’t saved sufficiently to supplement Social Security benefits, merely working longer and delaying the start of Social Security will boost your monthly income considerably if that is an option for you.

Now, about that lump sum pension.

Listening to a financial advice talk show and a caller asked this question. “I’m retiring and my employer offers a life annuity or lump sum. The annuity is $2,200 a month and the lump sum is $420,000. Which should I take?” With no hesitation the host said take the lump sum. Whoa‼️

That’s a lot of money and quite tempting I admit, but there are pros and cons in my view. If you take the annuity, you can’t outlive the benefit and it is insured by the Pension Benefit Guarantee Corporation. If the stock market takes a dive, it’s the plan sponsors responsibility to adequately fund the trust. Chances are the $2,200 will not increase over the years. In addition, if you die shortly after retirement no more benefits are payable unless you take a reduced benefit with a survivor annuity.

That’s a lot of money and quite tempting I admit, but there are pros and cons in my view. If you take the annuity, you can’t outlive the benefit and it is insured by the Pension Benefit Guarantee Corporation. If the stock market takes a dive, it’s the plan sponsors responsibility to adequately fund the trust. Chances are the $2,200 will not increase over the years. In addition, if you die shortly after retirement no more benefits are payable unless you take a reduced benefit with a survivor annuity.

If you take the lump sum, you have the money in your pocket. In theory if you invest and earn a return at least equal to that assumed by the pension plan, you can spend $2,200 a month and not outlive your money. But the market goes up and down and you must manage all that to have a steady monthly income and you must resist the temptation to withdraw a large sum of cash in your early years of retirement. In addition, that lump sum is based on your life expectancy when the calculation was made; so don’t plan on living longer ( or here for a really good return in the stock market).

Before you take the lump sum it may be wise to seek professional help as to where you will invest the money. In today’s environment a savings account or CD is not going to cut it.

OK, thanks Dick. My 66 year old eyes aren’t quite as bad as I feared, not to mention what they’re connected to.

LikeLike

Whoops, I used $3585 (not $3385) . And what scares me is, I checked it four times!

As Emily Litella used to say, Never Mind.

LikeLike

It was my fault. I had the wrong number in the chart. Just fixed it.

LikeLike

Dick, OK, I get it. Your statement says “if you live to your full life expectancy.” while the government’s statement includes the entire population, many of whom do not make it to the same “full life expectancy” based on the age of 70.

One last thing, in your chart, I did the arithmetic for age 62 and 67 and got the same total lifetime benefit as you did. But for age 70, I get $605,291, not $571,523.

LikeLike

I took the life expectancy of 14.07 years time 12 months = 168.84 months at $3385.00 per month to get $571,523.

LikeLike

Dick, This is from Social Security’s website: “As a general rule, early or late retirement will give you about the same total Social Security benefits over your lifetime.”

You say however, “If you live to your full life expectancy you will receive less in total than if you waited until age 70, but if you only live say ten years that changes.”

Please explain.

LikeLike

Let’s say you start the benefit at age 62 and live ten years. That lower benefit per month will be more in total than collecting the higher benefit starting at age 70, but only for two years. As you can see from the chart which is based 100% on Social Security info, they don’t give you the same total over an actuarial lifetime.

LikeLike

Simply put….Do believe a bird in the hand is worth more than two in the bush or not?

LikeLike