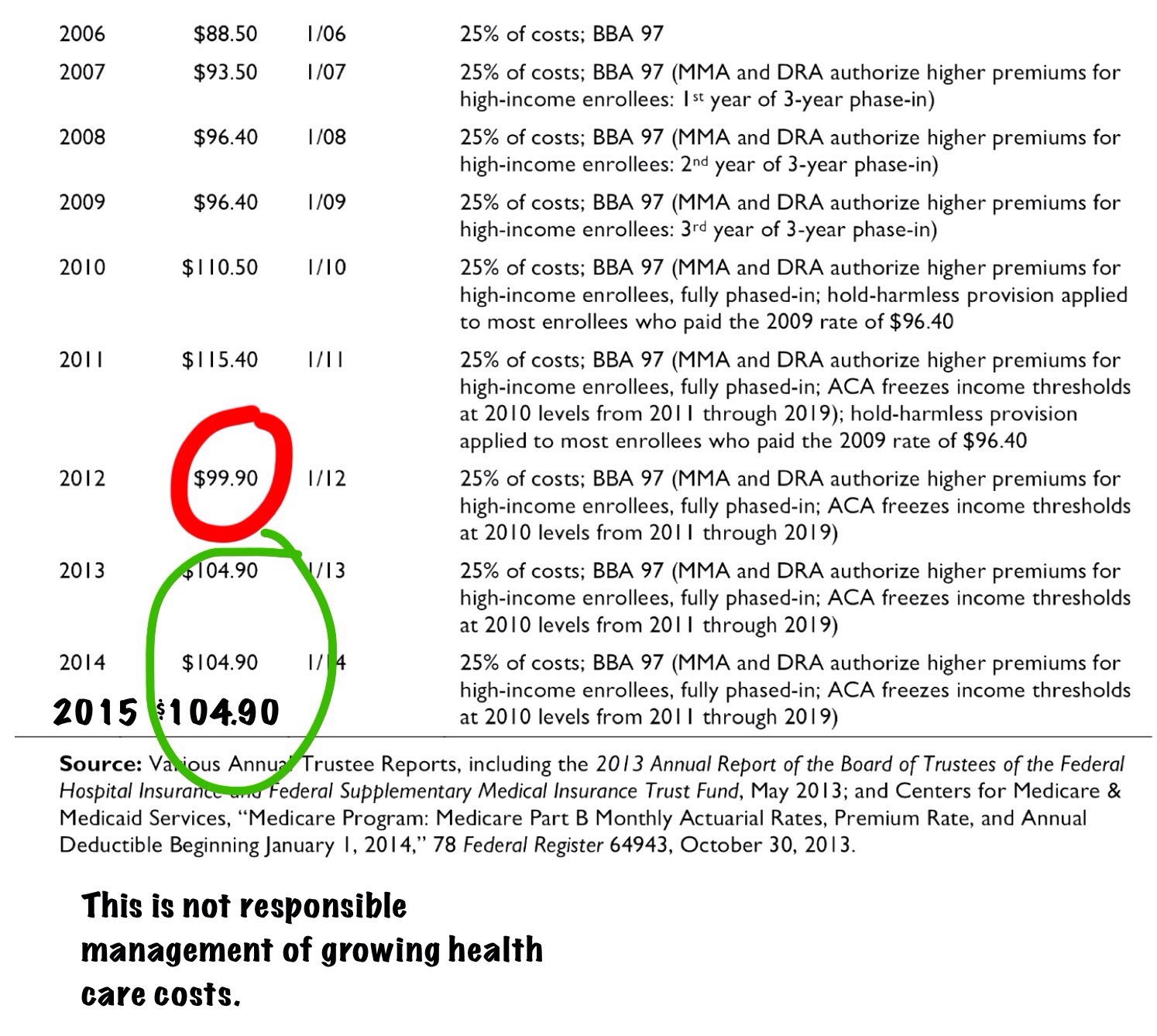

You may recall in the past several years I have commented that the low or no Part B premium increases (and even decreases) were questionable and in the long run not a great idea; a poor strategy and poor management.

It looks like the chickens are coming home to roost in 2016 with projected premium increases of up to 52%. This should make for interesting politics. Keep in mind that the Affordable Care Act froze the income levels through 2019 so more beneficiaries will be paying the higher premiums.

So much for all the success of Obamacare holding down health care costs.

Here is what the Medicare trustees are projecting:

- For incomes below $85,000 ($170,000 if filing jointly)—Part B premiums would rise from $104.90 to $159.30. (This is what newcomers to Medicare and those who pay premiums directly will pay next year if they are in the lowest income bracket.)

- For incomes between $85,000 and $107,000 ($170,000 to $214,000 if filing jointly)—from $146.90 a month this year to $223.00.

- For incomes between $107,000 and $160,000 ($214,000 to $320,000 if filing jointly)—from $209.80 a month this year to $318.60.

- For incomes between $160,000 and $214,000 ($320,000 to $428,000 if filing jointly)—from $272.20 a month this year to $414.20.

- For incomes above $214.000 ($428,000 if filing jointly)—from $335.70 a month this year to $509.80.

Now for the “good” news. Unless you are paying higher income premiums which are above the standard $104.90, your premium can’t be raised more than your increase in Social Security benefits which currently will be zero. Whoopee‼️ The 30% who do pay supplemental premiums must pick up the additional cost for the 70% who will not see an increase. Is that what you call the fair share?

What the Medicare Trustees say:

In 2015 the monthly Part B premium rate is $104.90. For determining an individual’s monthly premium rate, there is a hold- harmless provision in the law that limits the dollar increase in the premium to the dollar increase in an individual’s Social Security benefit. This provision applies to most beneficiaries who have their premium deducted from their Social Security benefit, or roughly 70 percent of Part B enrollees. Without the hold-harmless provision, beneficiaries would face a premium of $120.70 for 2016. However, because the cost-of-living adjustment for Social Security benefits is expected to be 0.0 percent for 2016, premiums would not increase from the 2015 level for those beneficiaries to whom the provision applies. Under current law, Part B premiums for other beneficiaries must be raised substantially to offset premiums foregone due to the hold-harmless provision, to prevent asset exhaustion, and to maintain a contingency reserve that accommodates normal financial variation. Accordingly, under the intermediate economic assumptions, the estimated monthly premium in 2016 for these other beneficiaries is $159.30, which is matched by general revenue transfers.

As you may know, your “friend” Professor Paul Krugman has recently confirmed to his followers of the left that the Medicare financing crises has ended. Thought you would like to see what one trustee said in response.

http://economics21.org/commentary/six-mistakes-paul-krugman-makes-about-medicares-finances

Amazing how you can read into data whatever you want to conclude/argue.

LikeLike

“So much for all the success of Obamacare holding down health care costs.” Obama care has very very very little to do with Medicare !!!!!!!!!!!

LikeLike

Not exactly, in fact most of the direct attempts to manage health care costs ONLY apply to Medicare.

LikeLike

Dick, thank you for keeping an eye on this for all of us. I am two years away from Medicare eligibility and, frankly, it doesn’t look good for me and my spouse.

LikeLike

It looks like you will have a very hefty premium not to mention the supplemental coverage cost.

LikeLike

Comment for malcontent50, if you are a federal annuitant, why are you paying for Part B of Medicare? The Federal Employee Health Insurance available to almost all federal annuitants is a much better deal (for the annuitant) than Part B of Medicare.

LikeLike

The FEHB plan only covers about 75% – 80% (at best) of all Part B type costs. The rest is out of pocket. With Medicare Part B and an FEHB plan as backup, in theory, you have no out of pocket medical expenses.

LikeLike

This is a bunch of crock..why are they raising Medicare premiums..when they should be raising Social Security benefits…they always try to get more money from the people..instead of giving us what we need to live on…i feel the politicians are getting a bit greedy with the money..we need someone who is “for the people” not “for themselves”…stop raising the Medicare premiums..give us more COLA raises..

LikeLike

If you are currently paying the standard $104.90 Medicare premium, you will not see an increase in your premium because you will not receive a COLA. Your SS benefit can’t be reduced because of Medicare premiums.

Where do you think the money will come from for all the things you want?

LikeLike

Dick,

Does this mean that going forward – beyond 2016 – for every new COLA we receive we will have to pay up to $159.30 before we can realize any net additional income?

R Richard Hoffer 2210 Pierce Lane Wharton, NJ 07885 973-328-1549 dickhoffer@aol.com

>

LikeLike

Not exactly. The $150.30 is only that high because 70% of those on Medicare are not paying any increase because there is no COLA.

LikeLike

To continue, in 2017 if there is a COLA and everyone pays more in premium that $159.30 could actually decrease. But for the 70% take the normal increase to $129.00 and add inflation to it for 2016. Let’s say it should be $135 for 2017. Then the COLA would have to be large enough to cover a premium from the current $104 to $135 in the example; pretty unlikely.

LikeLike

It appears my wife and I get the royal shaft here just as I am ready to turn 65. I am a federal annuitant under the “old” system (CSRS), as is my wife. I will never draw Social Security (neither will my wife). There’s no COLA in 2016 for federal retirees, and I will be a new Medicare enrollee for 2016 who will have to pay a supplemental premium. My wife already pays a supplemental premium for her Part B, and that will be going up 52%. Yeah…WE will definitely be part of the 30% subsidizing the 70%.

This “reckless management” of growing health care costs does not even begin to describe this debacle.

THIS CANNOT SUCK ENOUGH!!!

LikeLike

Well, I have to agree with you and part of the problem with these premiums is that instead of raising them gradually each year they (or as required by law), let them actually decrease in two years and not increase in three. That means there is a lot of catching up to do. In addition, if there is a COLA in 2017, it could easily be wiped out by Medicare premiums then.

LikeLike