When you consider what is included in ones modified adjusted gross income (MAGI), you don’t have to be a millionaire to pay high Medicare Part B and D premiums. A substantial required minimum distribution will put some people over the top, as will a good year of investment income.

In the early years of retirement pre-retirement income can throw a household into IRMAA charges.

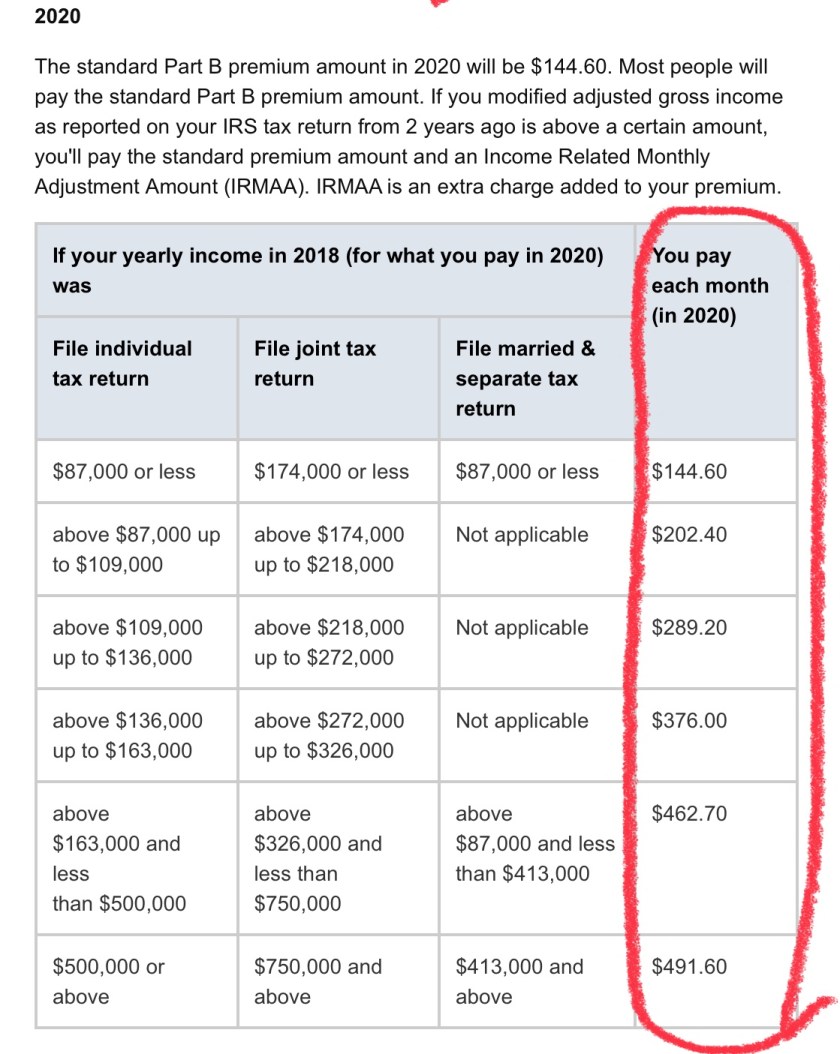

If you are a few years away from Medicare, these premiums are an important consideration in your financial planning.

Your MAGI is the total of the following for each member of your household who’s required to file a tax return:

• Your adjusted gross income (AGI) on your federal tax return

• Excluded foreign income

• Nontaxable Social Security benefits (including tier 1 railroad retirement benefits)

• Tax-exempt interest

Qualified distributions from Roth accounts are not counted as part of MAGI.

Starting in 2020, the income thresholds will be indexed to general price inflation, except for the top-level income thresholds of $500,000 for individuals and $750,000 married couples filing jointly. The top tiers will be indexed to inflation starting in 2028.

Prescription drug Part D premiums

Quinn. Most people are auto enrolled in part A and B. If you do not need part B (currently covered elsewhere) you do need to pay for Part B and must decline.

LikeLike

I can’t find anywhere on CMS or Medicare sites where it says Part B is auto enrollment.

LikeLike

Mr. Quinn:

I just went through this, this year … A bit over 3 months before the month of my 65th birthday, I was notified by Medicare that I was/would be auto-enrolled in BOTH Part A and Part B. However, at any time BEFORE the first of my birth month, I could “opt out” of Part B and thereby avoid the Part B premiums (and coverage).

But the default auto-enrollment is for both Part A and Part B.

LikeLike

I think from a financial planning prospective, it is more important to know that you do have to pay for Medicare in retirement. For 40+ years of working, I knew that I would qualify for Medicare by working and paying into it. I knew that Medicare was free. What I didn’t realize was that only part A was free. As a 18-year-old, part A did not mean anything to me nor what part A covered. Part D didn’t exist until I was into my 40’s. Even as I entered into my 50’s, I wondered why anyone would buy a Medicare supplement plan as advertised on TV. If I was told about the other parts of Medicare in either the retirement seminars or other publications, it still did not sink in. As I approached early retirement I finally understood that there were other parts of Medicare and it took me about a month of research after I retired before I understood it. One reason was that I knew of no one on Medicare to ask about it and I was still a decade away from being eligible for Medicare. I have 7 more years before I go on Medicare to figure out which supplement plans to buy. I fully understand that I need to pay for part B & D or get a private part C & D plan if I really want financial security in addition to having part A.

I also now know that there are co-insurance payments to be made, thanks to the TV commercials forced me into researching. But at the same time the TV commercials use the word FREE a lot in ordering supplies or equipment. I do not know what that is all about since I do not have the need for those products. But the advertising implies once on Medicare stuff is free. No wonder younger people want free healthcare.

I am sure a lot of people reaching age 65 expect Medicare to be totally free and believe that it would cover everything. Not everybody worked for companies that gave retirement planning. People do not save or plan for their retirement now. Why would they think about Medicare?

In fairness, when I was attending both the company and union retirement planning seminars, at about age 50, Obamacare was working its way through Congress. When asked about medical the answers were, this is how it worked in the past, nobody knew what Obamacare was going to do medical coverage in the future. It was anybody’s guess. Basically it was at that point that I determined that both Social Security and medical might not be around as I know it and that I might be on my own. I planned my retirement with that in mind.

LikeLike

Dwayne … your experiences and perspectives here are/were similar to my own. However, I did have reference to my mother’s experiences with Medicare and Supplements to provide me a bit of guidance before I got to retirement age. I just turned 65 this year, and did the Medicare, with a Medigap supplement.

Two things I would mention for you to consider while you have time before going on Medicare …

1.) There are more than Parts A through D to consider – and even those are changing. I would suggest going to Medicare.gov and looking through not just Medicare and Medicare Advantage (Part C) plans, but also check on the Medigap plans – there’s a whole additional “alphabet” of Plan parts for you to consider to best fit your circumstances.

2.) Something else for you to plan on for retirement – The actual costs/prices of ALL of these parts and plans are only going to increase! For example, just for the Part B premium – you are automatically “enrolled” in Part B when you reach age 65, unless you proactively decline – the INCREASE for 2020 went from $136*/month to $145*/month. That’s a 6.6% premium increase.

You may as well expect ALL of your Medicare and Supplement price increases for all of the future to run about 3 times the rate of general inflation. By the way, that was true in my mother’s time, and I’ve little doubt it will continue throughout OUR lifetimes.

* The “actual” published numbers for Part B premiums are $135.50 for 2019 and $144.60 for 2020. Problem is, when Medicare deducts that Part B premium from your Social Security payment, they don’t use fractional dollars – they round UP to the nearest whole dollar. Quite a sense of humor they have, publishing the $144.60, wouldn’t you say?

LikeLike

You are auto enrolled in Part A, not B

LikeLike

Thanks. I am also betting the medicare supplement plans (?) that my company offered will change or be non-existent in 7 years time. In a few years I will really look hard into because there is nothing I can do about except knowing that I will pay.

Pretty funny that they round up. That is like the gasoline tax of 9/10th of a cent. Like the pain will not be as bad if we call it less than a dollar.

LikeLike