There are advocates who see changing from the CPI-W to the CPI-E as a way to calculate the Social Security COLA. As you can see below, that is not the answer. Over 29 years the difference in the COLA was slight. And over some periods the CPI-E was less of an increase.

Some advocates want a guaranteed 3% annual COLA. That seems to me unfair to all working Americans. Why should one segment of our society have a guaranteed increase in income unrelated to actual price increases?

You can look at buying power or the loss of it on a macro basis, but that loss or lack thereof applies unequally across the retired population. Most retirees should have and could have planned for an increasing cost of living in retirement beyond counting on a COLA. But there are exceptions.

A COLA should be applied to those who most need it.

- That means that anyone who retires eligible for the maximum Social Security benefit is not eligible for any COLA for a period of time, say five years. Why? Because at that income level the individual should have other resources to deal with inflation.

- Any beneficiary who pays the highest income based Medicare Part B premium should not be eligible for any COLA. That reflects an income of $500,000 or more and certainly at that income level does not require a Social Security inflation increase.

From December 1982 through December 2011, the all-items CPI-E rose at an annual average rate of 3.1 percent, compared with increases of 2.9 percent for both the CPI-U and CPI-W. There are several reasons that older Americans faced slightly higher inflation rates over the past 29 years. First, older Americans devote a substantially larger share of their total budgets to medical care. The share of expenditures on medical care by the CPI-E population is roughly double that of either the CPI-U population or the CPI-W population. In addition, over the 1983–2011 period, medical care inflation increased significantly more than inflation for most other goods and services (5.1 percent annually for medical care, compared with 2.8 percent for all items less medical care). Second, older Americans spend relatively more on shelter, and during the last 29 years shelter costs have modestly outpaced overall inflation.

Although the CPI-E generally outpaced the official measures of inflation over the 1983–2011 timeframe, recent trends show different results. From 2006 to 2011, both the all-items CPI-E and the CPI-U rose at an average annual rate of 2.3 percent, while the CPI-W increased 2.4 percent. This turnaround was caused primarily by changes in the relative inflation rates of medical care and shelter, compared with the overall inflation rate. Specifically, the gap between medical care inflation and overall inflation has generally fallen since 2005, and shelter inflation has been rising slightly more slowly than overall inflation over the 2006–2011 period. Source: Bureau of Labor Statistics.

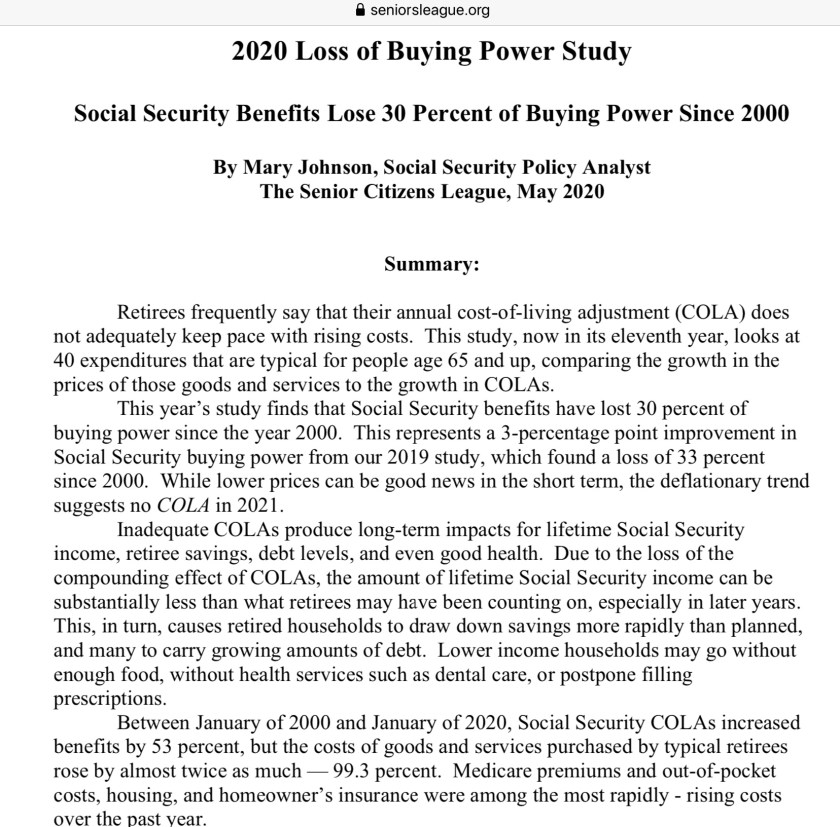

Source of above: The Senior Citizens League

Looks like the Majority do not understand ‘Seniority’ in life. SS Benefits are earned over a lifetime of working 45 to 50 years through economic disruptions and cycles caused by Global events such as Wars, natural catastrophes, Pandemics etc. These cycles always cause financial loss due to Job Loss, Investment losses and are most times beyond the control of most of us. (Except the Elected Government Leaders). The losses over 45-50 years of working causes many people to earn smaller SS payments than planned for. Once that age over 60 years or today even 50 kicks in the older Generation are not the preferred hiring candidates and cannot catch up on their income during a layoff to boost their future SS check.

Generally speaking, each Generation of society earns more money than their Parents did. With this fact known, our children and children’s children will make vastly more Money and thus more SS in retirement than we ever have.

Let this Generation be compensated for the forever rising Cost-of-Living. Most of us will pass on excess Wealth to our Children at our death, so they will always benefit from our inheritance and their greater earning ability than we ever had.

How many of us Graduated from College and immediately were offered a Job in the Tech. Industry starting at $106,000 per year with all the benefits such as free lunches in the Corporate Cafeteria, DC(Defined Contributions) plans of 18% in their retirement (Not a 401K)? How many of us were offered starting Engineer salaries of $77500.00 p.a.? How many of us were given a BMW, a TESLA or Lexus as their first car at College?(We, Mom and Dad even paid for their College Campus Parking Pass and their huge Auto Insurance.)

Our earned COLA’s are not at the expense of working Americans. Don’t treat the current working Americans as ‘Snowflakes’ and take pity on them. Their Generation never sacrificed and fought in Word War 11, Korea or Vietnam.

This current Generation is ‘not hard done by’ !

For me I do not even know why this is a Debate, except that you feel sorry for this current working class. If you or the Debaters want to take away any annual COLA increases to protect the future generations then I suggest you stop all COLA Increases at a fixed date, January 1st 2045. See what backlash and mayhem will follow?

LikeLike

John. I think you over generalize too much and miss the impact of years of inflation on salaries. Fact is the median HOUSEHOLD income in the US is only about $63,000 That includes every person living in the household. Those are the people who pay the SS taxes and our benefits. None of us earned our benefits. We paid taxes and got some benefits under the law unrelated to the taxes we paid. Investments go up and down, but over time always grow. Today’s economy is much harder to deal with and to have a steady job than we experienced and I started working out of high school in 1961.

LikeLike

Comment from BENEFIT JACK

The average Social Security benefit, according to this study, Increased 2.2% per year over the 20 year period. For comparison, the median household income in America also increased 2.2% per year over the same 20 year period.

Depending on what is in your market basket of goods, the inflation might be 99.3% for seniors as argued in the article or it might be much less.

How can that be?

Well, start with the massive shift from current workers to retirees in the form of Medicare Part D Rx Spending – where the federal government spent $95 Billion on Medicare Part D Rx in 2018. Across the ~ 46MM Medicare beneficiaries, that alone is $2,065 per capita – more than erasing the difference between 2.2% per year COLAs and the desired 3% minimum. Remember, there was no Medicare Part D in 2000.

The study confirms that the majority of the 60MM Americans who receive Social Security depend on their benefits for at least 50 percent of their total income. OK, whose fault is that? And, income is only one part of the calculation. How about accumulated wealth? Median (not average) net worth for individuals under age 55 is about $50,000. For those age 55+, the median is more than four times as high, > $200,000 (2016 Federal Reserve Data).

The percentage of older Americans living in poverty has declined from 35.2% in 1959 to 9.7% in 2018 (actual number is likely lower).

The percentage of children under age 18 has declined from 26.9% to 15.9%.

Really, you think it is smart policy to tax productive workers even more to fund even greater increases in senior’s benefits, benefits they clearly did not properly fund while they were working (Medicare PART A Trust Fund is scheduled to be exhausted in 2026, Social Security OASDI Trust Fund scheduled to be exhausted in 2032 – 2034).

Seniors better keep their eyes on maintaining what they already have. Everything else is Congress pandering for the grey-haired vote – looking to buy votes of current, older Americans and send the bill to those too young to vote, or generations as yet unborn.

LikeLike