First and foremost, I do not claim to be an expert investor or close to it. I am not qualified to give investment advice and I don’t do that, but I am happy with my retirement investments. To be sure, I may have done better… or worse,

I retired in 2010, so my 401k has had no new contributions since December 2009. Given I will soon be age 77, I have taken several required minimum distributions (RMDs).

But even with all those distributions my account balance today, June 26, 2020, is nearly 50% greater than it was the day I retired, the benefit of a long bull market. Now things have changed, but even so, after June 26, 2020 my account is still up for the year by a modest 0.22%.

As I said I’m no Peter Lynch, but I am aware of the need to be diversified, to gradually become less risky in investments as you near and enjoy retirement and to stay the course and not lock in your loses trying to flee a market crash. In both 2008 and 2020, I modestly added to equities in the market down turns, but that’s all I did. If I had been younger and working I would have directed all my new contributions into stock index funds.

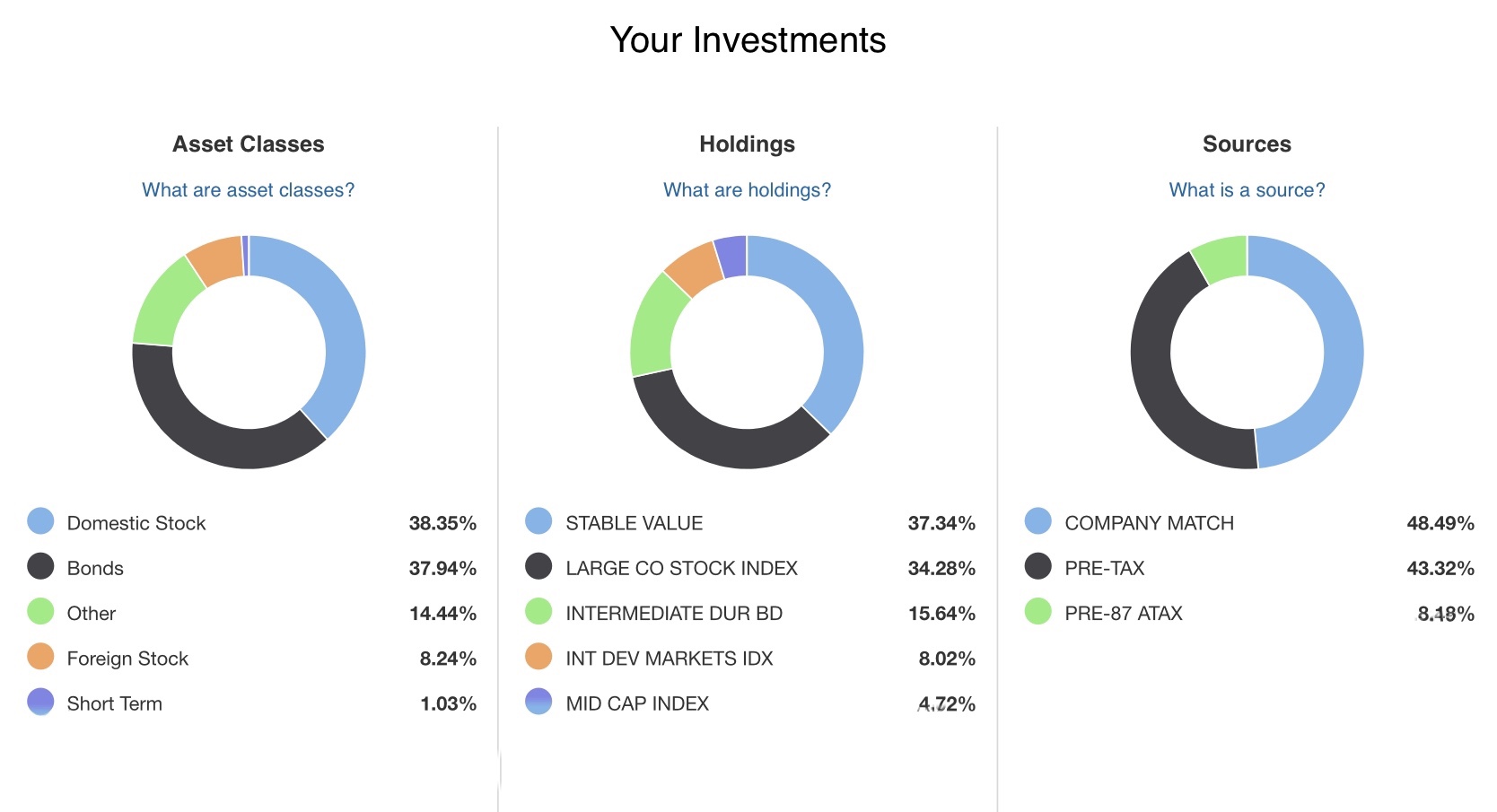

Here’s how I’m invested today:

Is this the optimum? Is it right? I hope so, but the point is I have a strategy that I can live with.

My wife and also retired in 2910, and also liive off pensions and Social Security, We are invested rather differently — all mutual stock funds. My wife’s IRA is probably most comparable to your investments, but it contains just one mutual stock fund, T..RowePrice New Horizons. For the last 10 years, it has increased by 20.94% per year (annualized figure due to TRP — includes RMDs).

LikeLike

Er, I meant 2010. Sorry for the typos. I forgot to answer your final question, “Do you have a strategy based on your age and circumstances?” Yes, I buy only mutual. stock funds, since a market downturn would not affect our modest life style. I think of our investments as an emergency fund, coveriing the possibility of requiring long term care.

LikeLike

Hi Richard! I always enjoy reading your comments, so thanks for sharing this about your investments. I was trying to figure out your split between stocks and fixed income by looking at your Asset Classes Graph and Data. The 14.4% allocation to “Other” made that difficult. What is “Other” for you? Thanks!

LikeLike

You consider what the optimal investment allocation might be for you, but you do it without a consideration of the size of your portfolio. What is appropriate for someone with a $10M net worth is not necessarily appropriate for someone whose net worth is $1M or less, and vice versa. An important question that must be answered is “what are the consequences if the market drops precipitously?” Thus, a 30% drop in equities for someone with all of his money in stocks is quite a different matter for someone with a net worth of $10M compared to someone with a net worth of $1M. The former can afford that (although it would be painful, he can still live comfortably), while it would affect the life style of the latter much more significantly. For a retiree, I suggest that the best thing to do is to safeguard an amount sufficient for normal living expenses through safe investments (if possible), and then consider what to do with the rest. Once you have enough to retire comfortably, the most important thing is to safeguard those funds, rather than to chase optimal yields. I suspect that your portfolio allocation does just that, but without a knowledge of total assets and necessary expenditures, any analysis is incomplete.

LikeLiked by 1 person

Okay. But it also must consider how the money is used or required to be used and when

LikeLike

I agree completely. We need to both consider how much we have and how/when it will be used to best assess investment strategies.

LikeLike

You present your investments and ask “Is this the optimum?” However, I think you are asking the wrong (and perhaps even a dangerous) question. I am confident that no matter what time period you select, you will look back and know for certain that your investments were not the optimum. With the benefit of hindsight, you will know that if you had increased your foreign stock exposure by X% and decreased your bonds by Y% (or some other combination of tweaks), you would have had a higher return with lower volatility. A desire for “the optimum” investments contributes to people chasing the next investment strategy that is proven (always through back-testing) to be better than whatever you are currently invested in. Perhaps it would be better to aim for investments that are “reasonable and prudent” while minimizing investing costs and tax implications.

LikeLike

The optimum for me that is. The main point being have some strategy that is right for you, especially considering risk tolerance.

LikeLike

Thanks for sharing. You said you retired in 2010, but it appears you continued to make contributions until 2019? Or maybe I am reading it wrong.

LikeLike

No, my last contribution was December 2009, thanks for pointing out my typo. All the growth is just from investment returns.

LikeLike