Many people planning retirement overlook the significant cost for Medicare premiums – let alone for supplemental coverage.

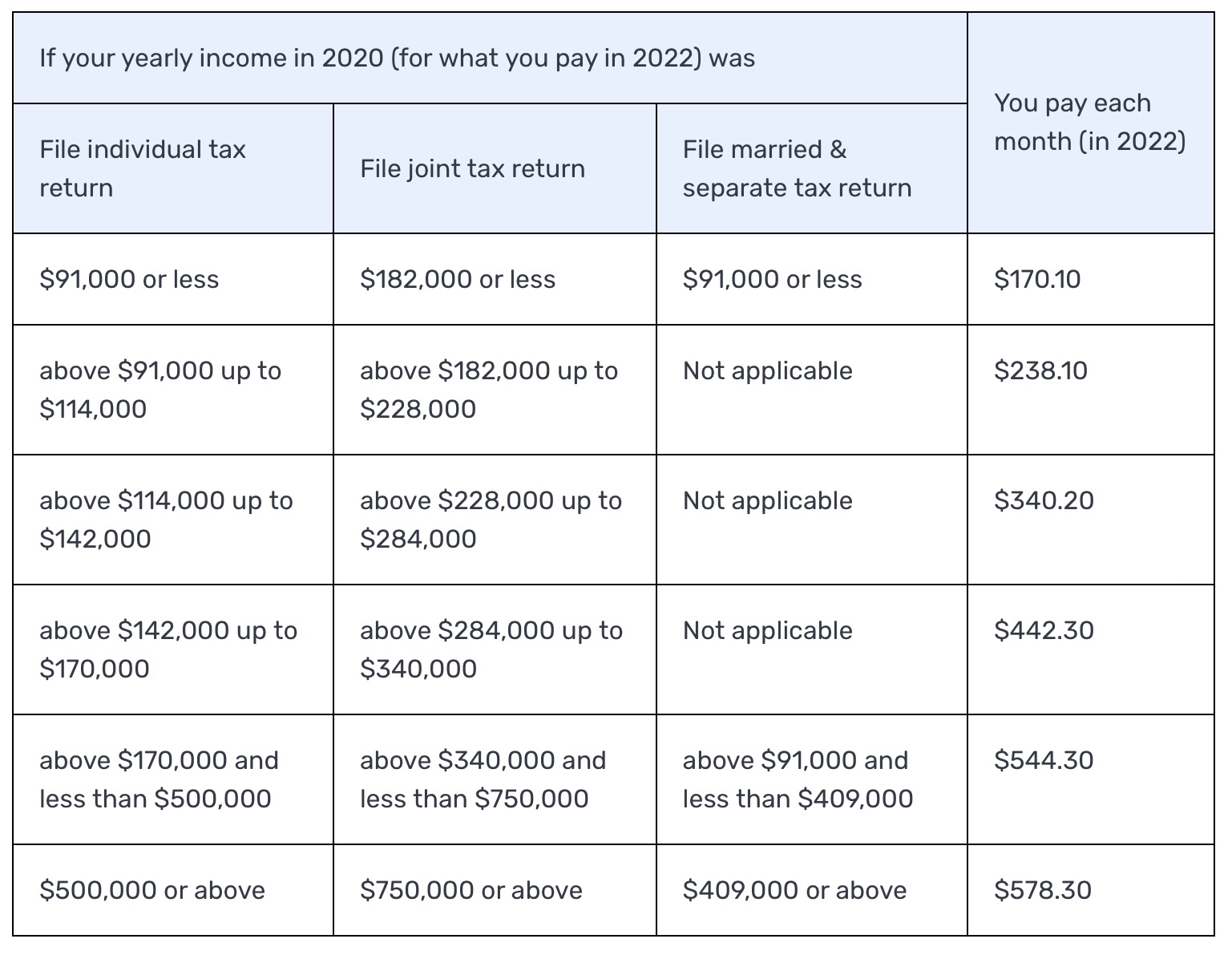

Some modestly higher income seniors pay quite a bit more for Parts B and D based on their modified adjusted income – MAGI.

MAGI is calculated as Adjusted Gross Income (line 11 of IRS Form 1040) plus tax-exempt interest income (line 2a of IRS Form 1040)

None of this is news to many people. HOWEVER, what may be overlooked is the disproportionate impact on a surviving spouse. For example, a couple with a MAGI just above $180,000 each pay $238.10 for Part B, but a surviving spouse with income of half that will still pay $238.10. It gets worse at higher income levels. Single individuals are at a disadvantage.

The big hit could come with the passing of one member of the couple and the survivor has more than half of the previous 2 person income. It could boost the survivor into an extra charge even though there is no real increase in income.

LikeLike

Not mentioned is that IRMAA becomes a factor in the year one turns 63 because of the 2-yr look back on income. One needs to begin paying attention to IRMAA MAGI 2-yrs BEFORE starting Medicare at 65.

LikeLike

It’s correct that IRMAA for 2022 is based on earnings in 2020 for example during which a new retiree may have working. However, you can appeal the amount and stopping work is a valid appeal.

LikeLike