Stating the obvious. What nonsense‼️

Don’t you love it when a study concludes that tax based benefits favor those who pay the most in taxes? 🙄

The Social Security formula favors the lower income worker and the percentage of income replacement declines with higher incomes – as it should be.

“Adequate incentives to save for retirement?” What could me more of an incentive than assuring your own financial security and perhaps that of a spouse?

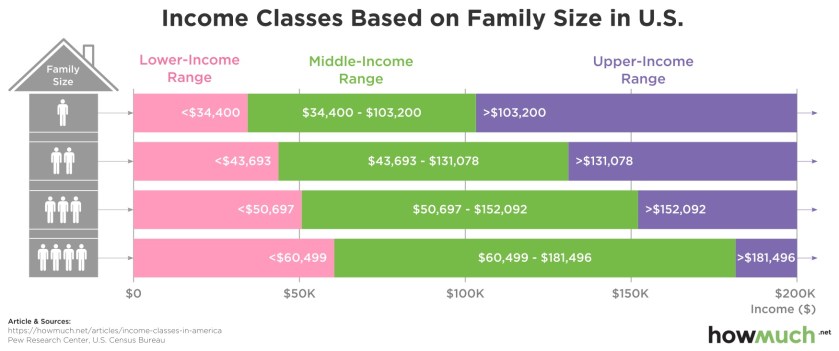

Middle class is thrown around pretty loosely, but what is it? Here is one version.

The Missing Middle: How Tax Incentives For Retirement Savings Leave Middle Class Families Behind also offers potential solutions that could enhance retirement security for middle class families.

The analysis indicates that more than half of the tax breaks for defined contribution (DC) plans and Individual Retirement Accounts (IRAs) go to those in the top ten percent by income. Also, the top 30 percent of workers by income receive 89 percent of the present value of tax benefits for DC plans and IRAs. This leaves a “missing middle” because the tax code offers meager benefits for these working Americans to save for retirement. At the same time, these middle class workers face rising costs in retirement, often lack retirement plans at their jobs, and need more than just Social Security income in retirement to maintain their standard of living.

The report’s key findings are as follows:

The current retirement saving structure suffers from a missing middle. The progressive nature of the Social Security benefit does much to prevent old-age poverty, but the level of income replacement from Social Security falls off far more quickly than private savings function to provide adequate retirement income for middle class workers.

Tax expenditures for various retirement programs are heavily skewed toward high-income earners. Some of this is due to the design of the tax breaks themselves, but outside factors, such as participation in employer-provided retirement plans and having the financial resources to save for retirement, also play a significant role.

The value of tax incentives for saving is much greater for those at higher income levels, who face higher marginal tax rates. These incentives are quite weak for much of the middle class. Additionally, those who are able to invest earlier and at higher levels enjoy a greater advantage from the deferral of taxation on investment gains.

The tax expenditures for retirement saving, oriented around the defined contribution system, give rise to inequities beyond income and wealth. Geographic and racial inequities related to retirement are both exacerbated by the tax incentives for saving.

Solutions to these inequities should focus on increasing participation in the retirement savings system and ensuring working families also receive adequate incentives to save for retirement. Some potential solutions could focus on building upon Social Security, either through benefit changes or allowing the program to integrate lifetime income options for savers.

Reforming the tax expenditures themselves, by eliminating the deduction-based system and replacing it with a refundable credit is another possibility.

Other solutions could focus on increasing access and participation in savings plans, which some states are doing for workers who lack workplace plans, thereby making it easier to participate.

Finally, curbing abuses of the existing system would ensure that the significant sums of federal tax revenue that are dedicated to retirement security are directed at generating retirement income.

“ Also, the top 30 percent of workers by income receive 89 percent of the present value of tax benefits for DC plans and IRAs.”

It’s hard to benefit from tax breaks when you’re paying no taxes.

LikeLike

And yet…

LikeLike

The study did not measuring who actually receives a reduction in taxes paid. The study is measuring the allocation of “tax expenditures” from a 10 year federal budget perspective. Since it only looks at the 10 year budget window, it does not accurately show the impact for 401k plans because it ignores most of the ordinary income taxation that occurs at payout; and, the lack of taxation for those who contributed on a Roth basis.

LikeLike

Appreciate the study, but 401k has delivered value to a much larger segment of US workers. Here’s the form 5500 data (1975 – 2019) from the Department of Labor:

# of Plans

1975 103k DB 207kDC

1983 172k DB (max)

2019 686kDC

# of Participants

1975 33MM DB 12MM DC

2008 42MM DB (max)

2019 109MM DC

# Active Participants

1975 27MM DB 11MM DC

1980 30MM DB (max)

2019 85MM DC

Assets

1975 $185B DB 74B DC

2019 $3,274B DB $7,433B DC

At its maximum, only 30 MM active DB participants. Most likely never vested as median tenure was consistently < 5 years for past five decades. Until 1989 (TRA 86 compliance), many DB plans used 10 year cliff vesting. See: https://www.psca.org/news/blog/make-retirement-plans-great-again

Progressive entitlements:

Social Security – Benefits favor low income (bend points, taxation of payments). Taxes = flat rate to wage cap.

Medicare HI, Part A – Same benefit once 40 qtrs of minimal FICA-Med taxes. Some low income are dual eligible). FICA-Med applies to all wages (no cap since 1993). New PPACA surcharges. Finally, only 43% of households paid income taxes in 2021 – funding source for Part B and Part D.

Yes, only 43% of US households paid federal income taxes in 2021!

LikeLike

I am not going to read this whole report to determine what the agenda this report is pushing. A few years back, I had the highest earnings ever for me due to massive amount of overtime. That happen to put me into the top 5% of US wage earners for that one year, and I believe a god status in some of the poorer countries. That income would have been in the upper green ban on two of the so called “middle income”. So whatever “middle” means, they are really stretching it.

So my silly question is where are the tax incentives for retirement savings for the lower income or the poor? This study is either a smoke screen to buy votes with the “middle class” or Wall Street lobbyist trying to get more money.

LikeLike

So I’m wrong because I was motivated to save for retirement because I knew that Social Security wouldn’t come anywhere close to paying for the lifestyle I want to live? And I’m wrong for putting almost all of it into Roth accounts so I don’t have to pay taxes when I take a distribution?

If I’m wrong, then where does “being right” get people?

It’s called “tax avoidance” and it’s a fun game to play. “Tax evasion”, on the other hand, can land you in prison. Choose wisely.

LikeLike