The reality is that in todays work environment a pension has little value. Most workers are better off with a 401k plan. Take a look.

- Less than 50% of all working Americans ever had a traditional pension

In a defined benefit plan, an employer can require that employees have 5 years of service in order to become 100 percent vested in the employer funded benefits (called cliff vesting). Employers also can choose a graduated vesting schedule, which requires an employee to work 7 years in order to be 100 percent vested, but provides at least 20 percent vesting after 3 years, 40 percent after 4 years, 60 percent after 5 years, and 80 percent after 6 years of service. Plans may provide a different schedule as long as it is more generous than these vesting schedules. (Unlike most defined benefit plans, in a cash balance plan, employees vest in employer contributions after 3 years.)

U.S. Department of Labor

Key Findings

https://www.caprelo.com/insights-resources/industry-trends/the-great-resignation-an-analysis-of-job-tenure-over-the-years/

- The average tenure for Millenials is 4 years, with the lowest tenure between the ages of 25-34 yrs old at 3 years.

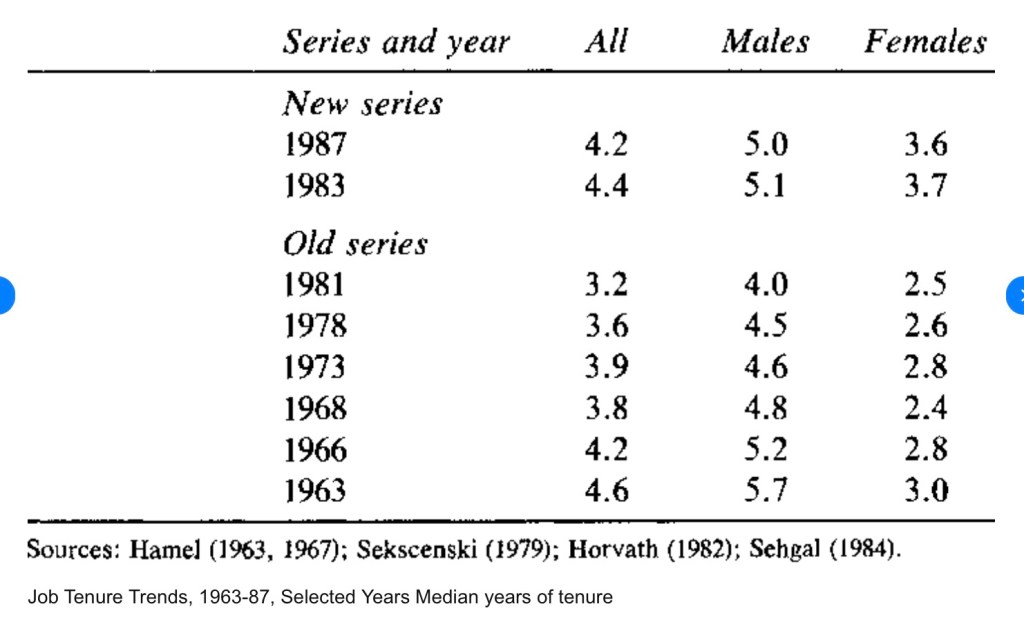

- The median years of tenure for people 18 years and older has dropped since January 2010 from 5.5 to 5.4 years in January 2020.

- The average years of tenure for women is lower than men at 4.7 years compared to 5 years.

- Manufacturing, Insurance and Healthcare facilities show the highest median years of tenure for the private sector jobs we analyzed—5.6, 5.5 and 5.4 years respectively.

- Management is one of the occupations with the highest median years of tenure at 6.3 years

The key to retirement for most workers is crafting their own income stream for the future.

I think of mining, or railroads right off hand. I was in Telecommunications for 30 years then Public Transportation. Both are unionized and offered good benefits. Unions are making a comeback, an opportunity for young workers perhaps!

LikeLike

Some states have gone to defined contribution plans, or are trying to.

1. It’s cheaper and simpler for the state.

2. They use the argument above; “It’s for your own good, for portability.”

States with DB plans also have a 457(k) optional additional plan equivalent to a 401(k) but with no employer match. Typically, it can be annuitized or, in my case, converted to an IRA. (The defined benefit plan is still mandatory, it’s not either/or .)

Very low participation rate, as I recall.

LikeLike

From my recollection, and this is easy to verify with annual reports,* most state and local public workers are not public workers at all. They are private sector workers on one of many positions they will occupy throughout their career. Public worker tenure is generally higher than private, but not remarkably so. About half of public workers don’t even work long enough to vest.

Only about twenty percent are “full career” employees (30+ years)

Generally, the participation rate of a public sector defined benefit is 100%. Participation is mandatory, including typically a five to ten percent employee contribution. But there are thousands who have pensions of only a few hundred dollars a month, and no retiree healthcare, because of their short tenure.

*”easy” is relative. The data is available, by law, for every pension system, but trying to search through and understand the data is a bear.

1. My info above comes from various studies or articles.

2. Since 2008-9 and the aftermath, public pensions have changed considerably, not for the better. (IMHO)

LikeLike

Public sector pensions – state that that is – are generally woefully mismanaged, way underfunded and overly generous because of the relationship between public unions and politicians. I sat on two state commissions to evaluate pensions and their provisions compared with private employers was outrageous ironically paid for by citizens who don’t have pensions

LikeLike

Most are. Way underfunded, that is, especially since 2001. Largely because they are not controlled by ERISA or something similar. Most Multi Employer Pensions are upside down also, for the same reason, and are being bailed out as we speak.

Some (New Jersey, esp.) were bad before bad became normal. They haven’t been contributing enough for over thirty years.

I totally disagree on the overly generous claim. On average, nationwide, higher pensions are offset by lower salaries. The outliers, on the high side, as one may guess, are on both coasts and Illinois. You might also guess why, and I would probably disagree there, also.* And in almost every state, pension formulas have been declining while worker contributions have been increasing.

Without all those pensions, and healthcare, the U.S. would be in much more dire straits than we are now.

Factoid, the CEO of America’s largest state pension fund has a high school degree. I haven’t looked in a long time, but, for a good time, look up her salary and bonuses. Somebody look it up so I don’t have to.

The common answer is “Blue States ” Would but that it were so simple.

LikeLike

NJ is the state I evaluated so i am very familiar. And, in fact salaries do not offset generous benefits. Look up the data from BLS and you can see.

LikeLike

apologia:

Implies not admission of guilt or regret but a desire to make clear the grounds for some course, belief, or position. “His speech was an apologia for …”

Merriam-Webster

Yes, New Jersey and California were/are among the most highly compensated states, along with Connecticut, New York, Illinois, Rhode Island, and Pennsylvania.

According to Biggs, California had relatively lower wages and higher pensions, and New Jersey the opposite. On average.

https://www.semanticscholar.org/paper/Overpaid-or-underpaid-A-state-by-state-ranking-of-Biggs-Richwine/87a87c8855dd9ac1ab11a4b9f41847a9f06d1ddf/figure/2

(this data from 2008-2012, national data. All states follow similar wage/benefit distribution pattern)

“On average”.

One caveat to rule them all.

New Jersey, California, Connecticut, New Mexico… Take your pick.

The lowest level public employees, those with little education or training, are the most over compensated relative to private sector workers, primarily due to their higher pensions and benefits. In order to reduce the ” average” public compensation to equal that of the average private compensation, this is where you must cut, full stop.

And the cuts must come from pensions and other benefits. I don’t believe there is popular demand or political will for these cuts.

LikeLike

I cannot find data for New Jersey specifically, but, is there any reason state workers should not be compared to employer establishments with 500 workers or more?

https://www.bls.gov/news.release/ecec.t03.htm

State and local workers total comp. $57.60/hr.

Wages 62%

Benefits 38%

…………………..

https://www.bls.gov/news.release/ecec.t06.htm

Private industry workers by establishment size.

500 workers or more total comp. $58.38/hr.

Wages 65.2%

Benefits 34.8%

…………………….

All private workers total comp. $40.23/hr.

Private sector 1-49 workers $32.32/hr.

It appears the dichotomy is not between public and private employees, but between large and small establishments. Large employers (500 workers or more) employ about 53 percent of U.S. workers.

LikeLike

SO YOU WANT A PENSION – WHY?

Let me ask another question. So, you want Social Security – why?

The answer is that “The key to retirement for most workers is crafting their own income stream for the future.”, and they are both streams of income in addition to other savings for retirement such as an IRA. However a pension is very hard to earn these days even if they are offered so at least take advantage of a 401K or a Roth. There is no loyalty provided by companies anymore so why wouldn’t employees job hop? At least with a 401K the employees can take their savings with them.

LikeLike

Dwayne is right. A pension is an income that one will not outlive. What scares a lot of people is that they will run out of money. A pension is insurance against that, while an IRA is not. The solution to this in an environment that makes earning a pension difficult is to convert part or all of saved funds to an annuity that pays a monthly income. This, of course, means that these funds are lost to the estate, but the insurance against outliving one’s money may well be worth it.

LikeLike

Very true, assuming your pension is from a viable company and well funded. I believe a steady income stream is essential. Taking perhaps a third of one’s assets for an immediate annuity is viable. I also contracted a stream of income with bond interest and dividends that don’t require touching the investment, but, of course, can be a bit variable.

LikeLike

The fact is that even in the past jib tenure was barely more than five years. Job hopping is actually not new. I have a good pension based on fifty years with the same company, but people like me are rare indeed.

LikeLike

Hello Sir Richard. I absolutely agree with the stick to it philosophy. Retirement is very easy. Find a company with great benefits to work at. Keep working at that place.

In my working life, I found 2 such companies and did just that. A Union steward mentioned to me once “How much would you have to have saved in order to pay the pension amount for life?” That fact, takes the stress out of having to provide your own funds after work.

I do have a question. In your experience what are the various work sectors that will provide a great retirement?

LikeLike

Sadly they are few, government employment is the best in terms if a pension and a heavily unionized industry probably next.

LikeLike