We can’t control what others do and we can’t stop misfortune from striking. But we can control our own actions. Those who are financially prudent will most likely enjoy success, even if events don’t always go their way.

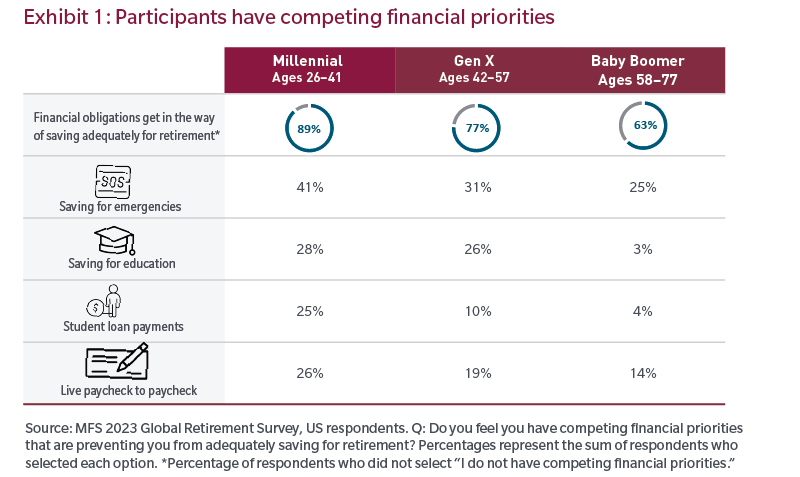

For many participants, competing financial priorities get in the way of saving adequately for retirement, further eroding retirement confidence. Exhibit 1 shows that while financial obligations affect retirement outcomes for all, there is an increased burden for the younger generations.

79% of plan sponsors say participants competing financial priorities have a major to moderate impact on their ability to save for retirement.4

Uncertainty over retirement is not just a problem for participants, it can also have implications for the sponsor. Studies have shown that financial stress can lead to lower productivity as well as increased turnover.3 And the uncertainty can make it difficult for employers to manage the overall workforce, potentially limiting opportunities for younger workers. Recent legislation has provided some flexibility to help participants address some of these challenges (more on this below), and sponsors should think about the issues facing their unique workforce and if there are policies or programs that could be employed to help ease these challenges.

“… Cost shifting health care expenses by way of higher employee premiums, higher deductibles and higher out-of- pocket costs. …”

In nominal dollars, certainly. In inflation-adjusted dollars, certainly.

However, those covered by Medicare and Medicaid and those in the public exchange receiving subsidies all pay LESS as a percentage of their income than they did 20 years ago – because of taxpayer subsidies and price controls.

For employer-sponsored plans, Americans pay a smaller percentage of the cost of coverage as out of pocket expenses (about 10%) compared to out of pocket spending in the 1970’s (30+%). That is, the premiums are much higher because the point of purchase cost sharing is a much smaller percentage of the charges. And, the charges are more than they should be because of government intervention – limiting the charges for Medicare, Medicaid, etc.

That is, the number and value of medical services has increased dramatically, and the government has interceded to cost shift much of the costs incurred by older Americans (who have the highest rates of utilization, as a group) to everyone else.

Don’t want to spend more on medical? Well, you could forego much of today’s medical science and go back to the 1950’s, 1960’s and 1970’s when people spent much less on medical, in part because people died at earlier ages. Not sure that is a tradeoff I want to make.

With respect to impediments to saving, we solved that problem in our 401k plan by coupling automatic features with “liquidity without leakage” nearly 20 years ago – creating the Bank of Dick, and the Bank of Jack.

Any employer who sponsors a retirement savings plan, like a 401k or a 403b can achieve the same outcome.

“… Cost shifting health care expenses by way of higher employee premiums, higher deductibles and higher out-of- pocket costs. …”

In nominal dollars, certainly. In inflation-adjusted dollars, certainly.

However, those covered by Medicare and Medicaid and those in the public exchange receiving subsidies all pay LESS as a percentage of their income than they did 20 years ago – because of taxpayer subsidies and price controls.

For employer-sponsored plans, Americans pay a smaller percentage of the cost of coverage as out of pocket expenses (about 10%) compared to out of pocket spending in the 1970’s (30+%). That is, the premiums are much higher because the point of purchase cost sharing is a much smaller percentage of the charges. And, the charges are more than they should be because of government intervention – limiting the charges for Medicare, Medicaid, etc.

See: https://www.aei.org/op-eds/medicares-price-setting-rules-an-alternative-perspective/

That is, the number and value of medical services has increased dramatically, and the government has interceded to cost shift much of the costs incurred by older Americans (who have the highest rates of utilization, as a group) to everyone else.

Don’t want to spend more on medical? Well, you could forego much of today’s medical science and go back to the 1950’s, 1960’s and 1970’s when people spent much less on medical, in part because people died at earlier ages. Not sure that is a tradeoff I want to make.

With respect to impediments to saving, we solved that problem in our 401k plan by coupling automatic features with “liquidity without leakage” nearly 20 years ago – creating the Bank of Dick, and the Bank of Jack.

Any employer who sponsors a retirement savings plan, like a 401k or a 403b can achieve the same outcome.

LikeLike