Nobody stole or misused the Social Security funds, Congress hasn’t used the funds for other spending, people illegally collecting benefits is a myth.

The Trust is invested in interest paying Treasury bonds.

Social Security cannot run out of funds.

Social Security isn’t literally “going broke,” but a key part of it—the trust fund—is projected to run low. Here’s what’s going on in plain terms:

1. How Social Security is funded

The U.S. system (managed by the Social Security Administration) mainly relies on:

- Payroll taxes (workers + employers each pay 6.2%)

- Interest on trust fund reserves

- Some taxation of benefits

For decades, it collected more than it paid out, building up a surplus in the trust fund.

2. What changed

Now the system is paying out more than it collects. The main reasons:

Aging population

- Baby boomers are retiring in large numbers

- People are living longer and collecting benefits longer

Fewer workers per retiree

- In 1960: ~5 workers per retiree

- Today: ~2.7 workers per retiree

- Heading toward ~2.2 in coming decades

That means fewer people paying in to support each beneficiary.

3. The trust fund drawdown

The surplus built up over time is stored in the Social Security trust fund (invested in U.S. Treasury bonds).

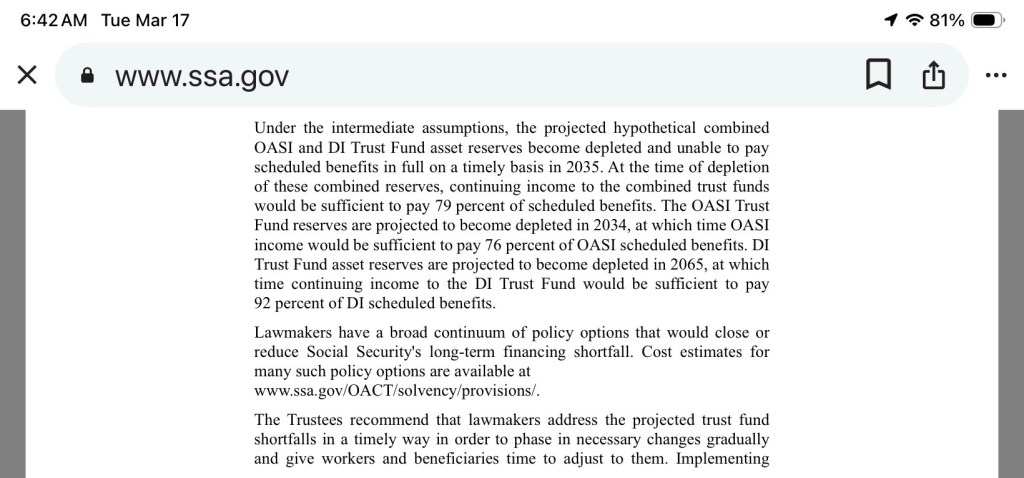

- Since around 2021, Social Security has been using that reserve to cover the gap

- At current trends, the trust fund could be depleted around the early–mid 2030s (per Social Security Trustees reports)

4. What “running out” actually means

Even if the trust fund is depleted:

- Payroll taxes keep coming in

- That would still cover about 75–80% of promised benefits

- Recent legislation making some SS benefits income and tax free make this situation worse by lowering the income taxes that go into the SS Trust.

So:

- ❌ Not zero benefits

- But automatic benefit cuts (~20–25%) if nothing changes

5. Why it wasn’t fixed earlier

This has been known for decades, but solutions are politically difficult because they involve tradeoffs like:

- Raising taxes

- Cutting benefits

- Raising the retirement age

- Some combination of all three

6. Common proposed fixes

You’ll hear ideas like:

- Increase the payroll tax rate slightly

- Raise or eliminate the income cap on Social Security taxes

- Gradually increase full retirement age

- Reduce benefits for higher earners

- Some combination of changes are necessary, changes that share the burden between working Americans and current beneficiaries. Current beneficiaries are enjoying promised benefits when for decades they should have been helping with the funding gap.

Bottom line

Social Security is under strain mainly due to demographics (aging + fewer workers). It’s not disappearing, but without policy changes, benefits will likely be reduced in less than a decade.

Congress should have addressed the well-known problem decades ago when making the necessary changes would have been minor, gradual and painless. The annual SS Trustee Report has been urging this for many years, but Congress fearing the ignorant backlash of voters has failed to act.

Misuse includes spending money, assets, prior contributions to buy votes.

LikeLike

The Supplemental Security Income program is designed to fill gaps in Social Security for the lowest income retirees. It is more Congressional spending without bothering to raise revenues via proper funding – further increasing our annual deficits and our $39+ Trillion national debt.

It is how Congress spends more money that we do not have, how they misuse their authority with an eye on buying votes, when they don’t want to make more obvious changes in Social Security which would further accelerate the exhaustion of the OAS Trust Fund.

Congressional Democrats and Republicans recently introduced the SSI Restoration Act of 2026, which would expand eligibility and increase benefits for Supplemental Security Income (SSI), a $63 billion cash assistance program that served 7.4 million elderly and disabled Americans in fiscal year 2024. The bill updates many of the program’s eligibility requirements, some of which have not been updated since the program’s inception in 1972.

This includes 1) increasing benefits by raising SSI’s countable asset limits and indexing maximum monthly SSI payments to 100 percent of the federal poverty level, 2) raising income disregards—the amount of earned and unearned income that is not counted when determining SSI eligibility—and 3) removing in-kind support and maintenance (ISM)—food or shelter that another individual provides to the beneficiary—from countable asset limits.

The Roosevelt Institute estimated that a 2024 version of the bill would significantly reduce poverty among households on SSI, but cost roughly $61 billion per year—nearly doubling current SSI spending.

As AEI scholar Mark Warshawsky argues, expanding SSI should be coupled with reforms “that will balance costs with savings, improve fairness and incentives to work, and ease administrative burden.” Warshawsky’s recommendations include imposing a maximum family benefit limit, eliminating asset exclusions for life insurance, capping home value exemptions, and eliminating dedicated accounts for young SSI recipients.

The New SSI Bill’s Price Tag – $610 Billion – to be added to annual deficits and national debt.

LikeLike

Your last paragraph says years ago changes would have been minor, and painless. If that were true it would have been done. There’s nothing minor or painless about the changes needed. Gradual I would grant. It’s a costly program and I enjoy being a recipient but paying in not so much.

LikeLike

“Nobody stole or misused the Social Security funds”.

Disagree. Misuse is defined as: “Misuse is the incorrect, improper, or illegal use of something, often involving misapplication, mismanagement, or using an item for a purpose for which it was not intended.”

Few government programs are as poorly managed, where various administrations have approved unfunded improvements in benefits in order to buy votes. Starting with the first Social Security beneficiary, Ida Mae Fuller. Because of a number of amendments to accelerat the payment of benefits, signed into law by President FDR, she paid a total of $24.75 in FICA taxes and received $22,888.92 over a 35 year period after retirement at age 65.

From the Social Security Administration website:

The 1939 legislation … provided a new method of computing benefits, based on average monthly earnings instead of on cumulative wages. The net effect of the 1939 amendments was to increase the annual cost of benefits payable during the early years. In addition to these changes in benefits, the 1939 amendments made basic changes in the financing of the Social Security program by establishing the OASDI Trust fund and changing prior law provisions that would have resulted in the accumulation of a huge reserve fund over the years, similar to the reserves built up by private pension plans. The new legislation was designed to constrain the accumulation of reserves and, in effect, to move the financing of the program toward “pay-as-you-go” financing. This change in the reserve concept allowed the immediate payment of benefits to retired workers and to their dependents and survivors without increasing Social Security tax rates. This change in financing also permitted a 3-year postponement of the increases in the Social Security tax rate that had been scheduled for 1940.

Other recommendations included in the 1939 legislation were an earlier start of benefits, in 1940 instead of 1942, and a change in “quarters of coverage” in terms of how long someone had to work (shortening the period) in order to qualify for a benefit.

Social Security is under strain mainly due to demographics (aging + fewer workers).

Disagree. Social Security would have been able to cope with aging and fewer workers until President Carter made changes in 1977 that damatically increased benefits, without appropriate funding (knowing full well the coming generation of Baby Boomer retirees). He indexed past wages for inflation and gave us the COLA (instead of annual decisions on whether to increase benefits and the taxes that would be needed for funding). Idiots like President Biden made funding worse with his vote buying scheme benefitting public sector workers with his “Social Security Fairness Act.”

Other Presidents acknowledged the issue but sat on their hands:

Social Security Reform Over the Last 30+ Years:

• November 5th, 1993: President Bill Clinton, by Executive Order #12878, created the Bipartisan Commission on Entitlement Reform (the Danforth Commission) to evaluate entitlement programs – specifically Social Security and Medicare. The Commission never reached consensus and couldn’t get all members to agree on even an Interim Report. Subsets of the commission members made their own proposals. None gained any traction, nor action. See: http://www.presidency.ucsb.edu/ws/index.php?pid=61571

• February 5, 2005: President George W. Bush made a reform recommendation to add personal accounts and change the COLA. These proposals triggered great criticism, and no action was taken. See: https://georgewbush-whitehouse.archives.gov/infocus/social-security/ See also: https://georgewbush-whitehouse.archives.gov/news/releases/2005/04/200504…

• April 27, 2010: The bipartisan National Commission on Fiscal Responsibility and Reform (often called Simpson-Bowles) met to recommend fiscal reform, including recommendations to reform Social Security. Despite widespread popular support, the report failed to get enough support to send it to Congress for approval.

• June 1, 2016: President Barack Obama, nearing the end of this second term, reminded us that Social Security’s finances needed strengthening. “We should be strengthening Social Security… it’s time we finally made Social Security more generous and increased its benefits so that today’s retirees and future generations get the dignified retirement that they’ve earned.” No proposal was ever made. See: https://obamawhitehouse.archives.gov/the-press-office/2016/06/01/remarks…

• In an October 2017 GAO report, nearly ten years ago, GAO noted: “… (we) better ensure a secure and adequate retirement, with dignity, for all.” But, it offers no plan of action other than another committee. And, of course, more committees are what Congress is proposing today – both our annual deficit and national debt and entitlements.

“Congress should have addressed the well-known problem decades ago when making the necessary changes would have been minor, gradual and painless. “

Disagree and Agree. Disagree in that Congress created this problem by repeatedly amending the plan to improve benefits without increasing funding, where the benefits are now far, far beyond the initial intent to ensure seniors avoid poverty. Agree that Congress, having decided to use the program to buy votes, should have long ago tied funding changes, including an annual adjustment, to ensure that the program was sustainable for the next 1, 3, 5, 10, 25, 50, 75 and indefinitely (lives in being) so as to create a modicum of intergenerational equity.

Instead, they are playing off today’s seniors (by lying to the majority by saying that they earned their benefit) against Americans too young to vote and generations unborn who will have to fund benefits awarded to generations (greatest generation, silent generation, oldest boomers) who didn’t properly fund them.

LikeLike

You surely have a unique way of looking at things, but the trust funds were still not stolen or misused.

The entire program was and is mismanaged because changes were made without adequate funding and taxes were not adjusted to cope with changing demographics.

But many people are convinced Congress stole funds and if that had happened, all would be well AND THAT IS NOT TRUE.

LikeLike

Misuse = Mismanagement

And, we are NOT talking about only the failure to take action since Reagan and the 1983 Social Security Amendments Act. We are talking about abuse in terms of changes to buy votes, to improve benefits, to reduce reserve accumulations and to send the bill to generations then too young to vote and generations yet unborn.

Start with FDR, not Bush 1 or Clinton (following Reagan action). Consistent, deliberate, intentional misrepresentation and misuse of the program.

LikeLike