I wonder how many workers read this statement and take it seriously?

Social Security benefits are not intended to be your only source of income when you retire. On average, Social Security will replace about 40 percent of your annual pre-retirement earnings. You will need other savings, investments, pensions, or retirement accounts to live comfortably when you retire.

Source: Annual statement sent to workers.

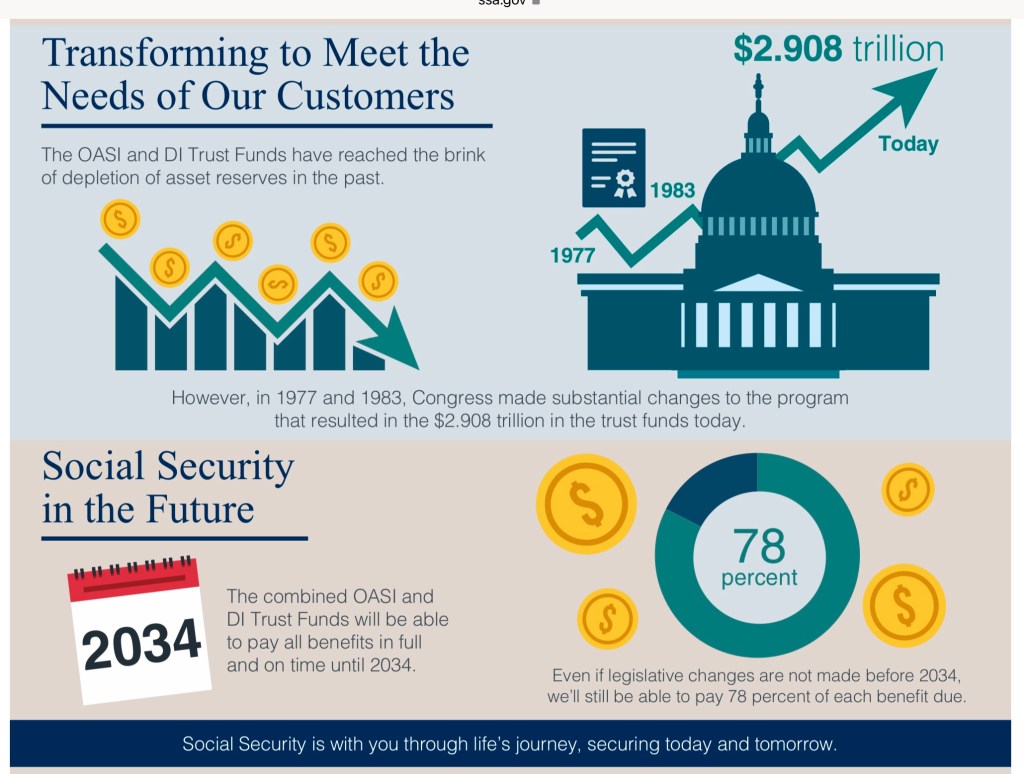

The explanation of the state of the Social Security trusts has been removed from the annual statement and replaced with this link.

When you click on the link, you get this explanation.

But that explanation is misleading. There is no combined trust fund(s), that is hypothetical. The old age survivor trust is what matters to most Americans. And the graph implying the trust balance is growing is also misleading. Congress has not taken action to fix the old age trust in nearly 30 years.

Those of us who have studied SS know that almost no one pays enough in FICA taxes, (including employer FICA taxes paid) to cover lifetime benefits collected if they live longer than 8 years after starting SS retirement benefits. I will have all FICA taxes paid, in inflation adjusted 2018 dollars, ( the year I started SS benefits) back in just 66 months. By Dec 2032 my wife and I will collect $241,048 in total SS benefits, not counting COLAs, 2021 dollars. That is 2.7 times my FICA taxes paid. I have other retirement income, so I will be ok with any adjustment to my monthly SS income. I think Congress will change the law and just fund any shortages with borrowed money like they are doing with everything else.

LikeLike

Thanks. Adjust your calculation for earnings foregone, and your estimate that “almost no one” will change to almost all whose AIME is in excess of the second bend point, as well as those who die prior to aging in, or soon thereafter. Assuming a 6% rate of return, and adjusted for taxes, I will never recover 1 cent of the contributions from my take home pay – no matter how long I live.

LikeLike

What has happened during the last 50 years that has changed what I learned in high school that the 3-legged retirement stool that SS would cover 1/3 of your expenses to now SS covers 40% of your expenses in retirement?

LikeLike

40% for low and moderate income, but that declines as income rises

LikeLike

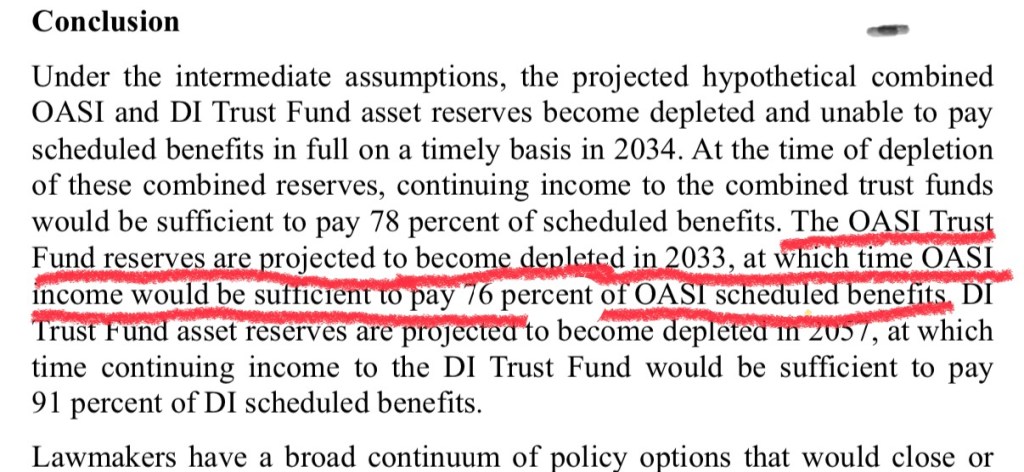

How will 76% of benefits be paid in 2034, if funds are depleted in 2033? Are we re-defining what depleted means?

LikeLike

I coming payroll taxes are sufficient to pay benefits at the 76% level.

LikeLike

So, do you know what happens if Congress, a la 1983, waits to the last minute but, this time, fails to act before the Social Security OAS trust fund is exhausted)?

Many assume that there would be a cut in benefits to match the payroll taxes. However, the correct answer is

… no one knows. No one knows because two laws apply and they are apparently in conflict:

– Under the Social Security Act, beneficiaries would still be legally entitled to their full scheduled benefits (at least until Congress says they are not), and

– Under the Antideficiency Act, the federal goverment is prohibited from spending in excess of available funds, so the Social Security Administration (SSA) would not have legal authority to pay full Social Security benefits on time.

I’m happy to bet on this, however. I’ll put it all on red – raising taxes. I don’t think there is anyone in Congress who has the courage to reduce benefits – other than perhaps reduce the rate of increase. Changing the system to incorporate a needs basis makes it into a welfare program and, why would you save anything or seek an employer who offers a pension plan if all it will do is reduce your Social Security benefit. So, I expect to see new surtaxes (a la IRMAA), and an increase in FICA taxes as well – because, seems clear that Congress is very willing to raise taxes on people too young to vote and generations yet unborn.

LikeLike

I am betting that Congress will fund the shortfall through the general fund like they did with Medicare since payroll taxes does not cover the expenses.

LikeLike

Medicare Part A is a trust fund running out of money. Parts B and D were never funded, but just general revenue. Trying to fund SS from general revenue is a big mistake.

LikeLike

I didn’t pay attention to capital graph when I first saw that chart a week ago. That is very misleading. Yes the fund has grown to almost $3T, but one might also consider it to be the liabilities too. The Trustees report for years has been warning that tax collection will no longer meet the liabilities in the mid 2030’s. Now I have an idea of how short Social Security will be in 2034. It’s about 24% of $3 trillion or about $720m.

LikeLike